M&A Bytes: Share Sale vs Asset Sale

Are you buying the company or just what’s inside it? One decision. Major Consequences.

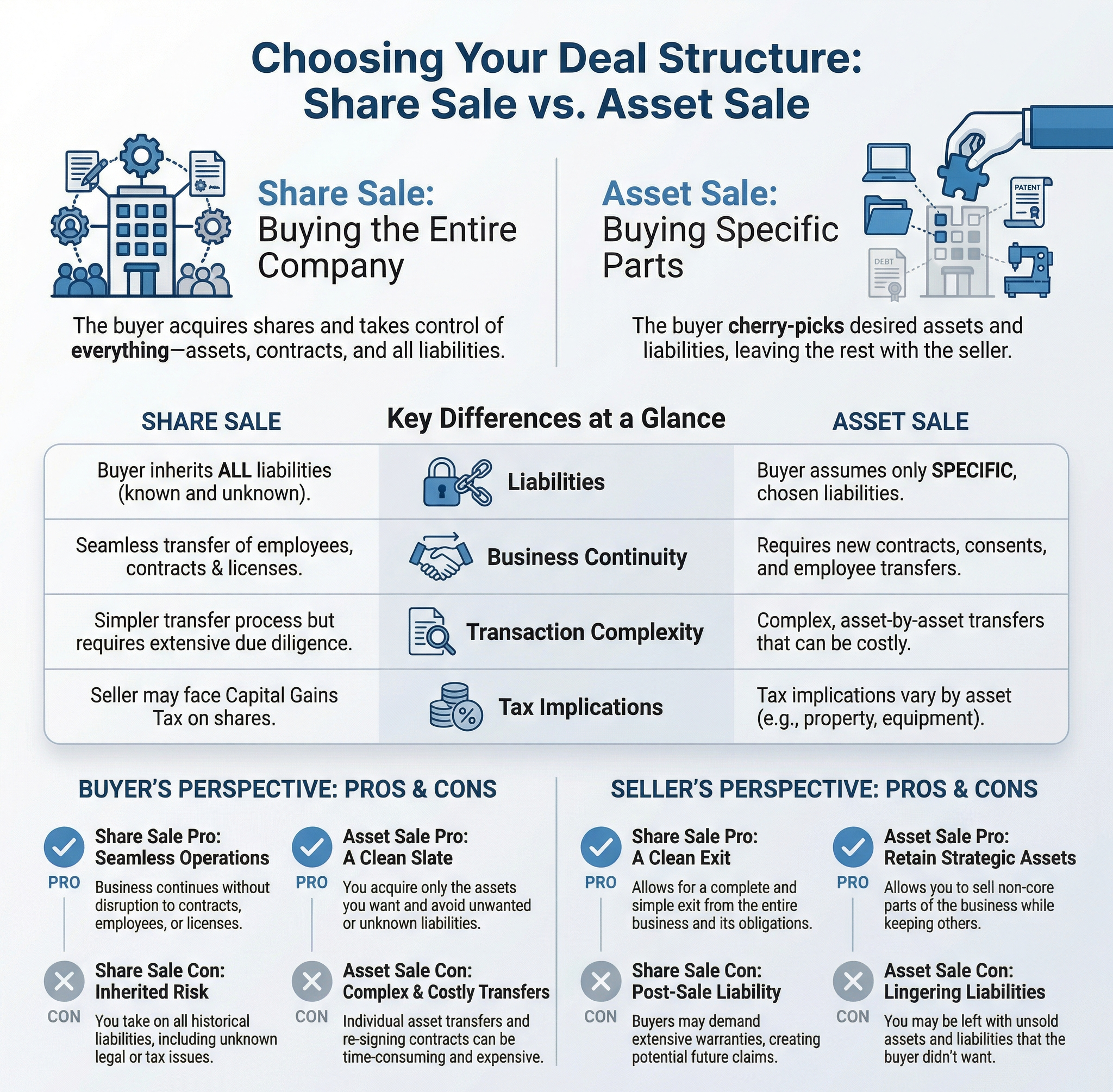

Every business acquisition starts with a critical question: Are you buying the company, or just the assets that matter to you?

- In a Share Sale, you acquire shares in the company — this may be 100% of the shares (full control) or a partial share sale. In either case, you take on the company’s assets, liabilities, contracts and its full corporate history.

- In an Asset Sale, you selectively acquire only the assets and operations you want, leaving the rest with the Seller.

Key Differences between Share Sale & Asset Sale:

| Aspect | Share Sale | Asset Sale |

|---|---|---|

| What’s Being Sold/ Scope | Buyer acquires ownership of shares and gains control of the entire company, including all assets and liabilities. | Buyer acquires specific assets and liabilities (e.g. properties, equipment and machinery, etc.). Seller retains the rest. |

| Contract Parties | The shareholder and the Buyer. | The company itself and the Buyer |

| Tax Implications

(For general information only. Please seek professional advice for actual tax implications.) |

|

|

| Consents & Approvals |

|

|

| Employment | No change of employer, employee consent is not required. |

* Note: Employees who reject equally favourable terms may lose entitlement to termination benefits. |

| Due Diligence Considerations |

|

|

| Warranties & Indemnities |

|

|

Pros & Cons for Buyer and Seller:

Share Sale

| Party | Pros | Cons |

|---|---|---|

| Buyer |

|

|

| Seller |

|

|

Asset Sale

| Party | Pros | Cons |

|---|---|---|

| Buyer |

|

|

| Seller |

|

|

🔑 Key Takeaway:

Choosing between Share Sale and Asset Sale is more than just a technical decision – it affects your legal exposure, tax implications, operational control and transaction complexity.

In Essence:

Disclaimer: The content of this article is intended for general informational purposes only and does not constitute formal legal advice.

Our Corporate team regularly advises local and international corporations on mergers and acquisitions (M&A), cross-border transactions, joint ventures, and corporate restructuring. We also provide comprehensive support for shareholders’ agreements and general commercial advisory to help businesses navigate the Malaysian regulatory landscape.

For legal assistance or further inquiries regarding your corporate matters, please feel free to contact us.