Corporate & Commercial

- July 28, 2026

When it comes to completing a deal, timing isn’t just about the date – it is about the conditions.

Do you know the difference between what must happen before closing, and what can happen after?

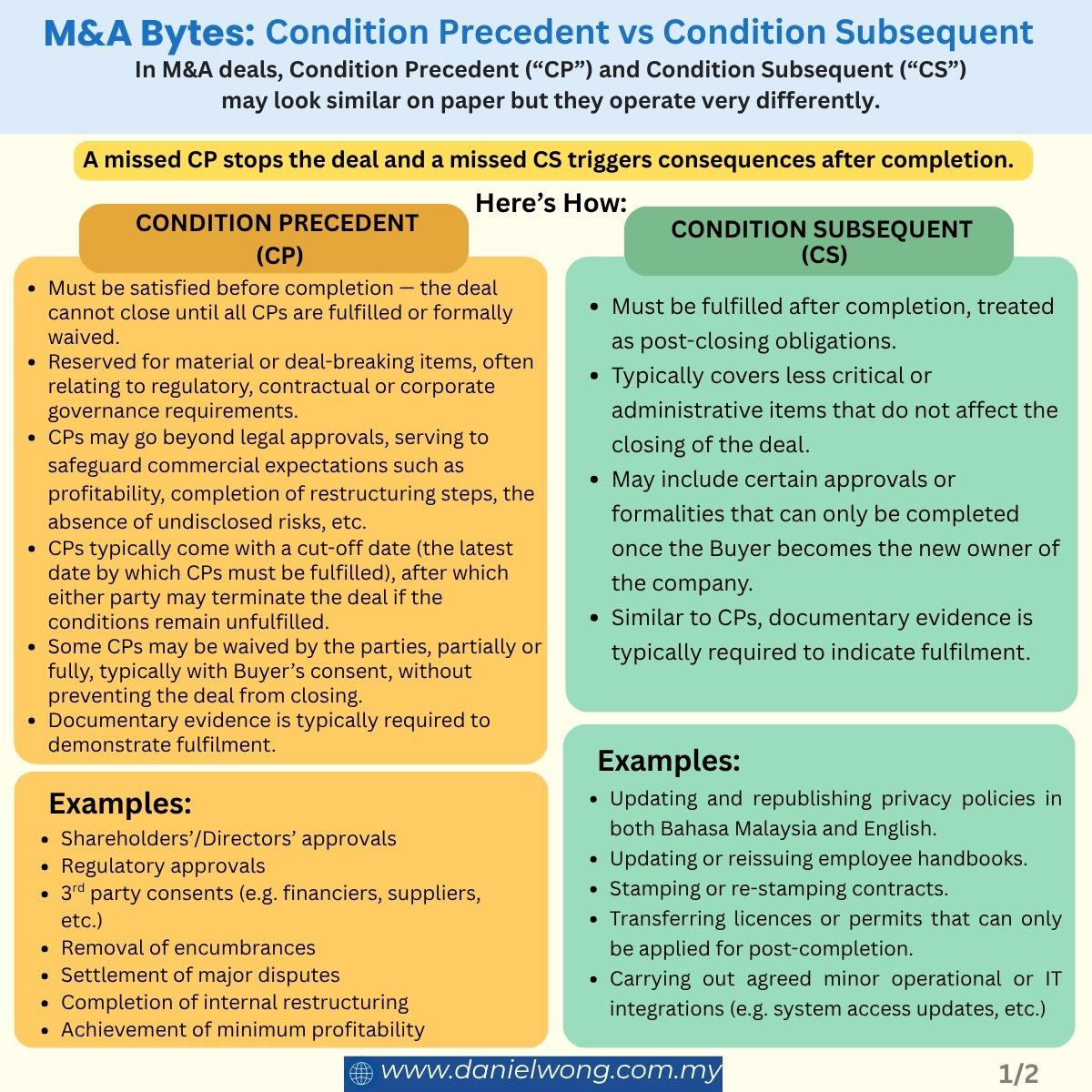

In M&A deals, Condition Precedent (“CP”) and Condition Subsequent (“CS”) may look similar on paper, but they operate very differently. A missed CP stops the deal, and a missed CS triggers consequences after completion.

Find out how these conditions impact your M&A transactions.

What are Conditions Precedent?

Condition Precedent

Conditions Precedent (“CP“) exist to ensure, amongst others, that the essential approvals, financial clean-ups, housekeeping matters, restructurings and third-party consents are completed before the buyer is locked in.In essence, CP:- Must be satisfied before completion – the deal cannot close until all CPs are fulfilled or formally waived.

- Reserved for material or deal-breaking items, often relating to regulatory, contractual or corporate governance requirements.

- CPs may go beyond legal approvals, serving to safeguard commercial expectations such as profitability, completion of restructuring steps, the absence of undisclosed risks, etc.

- CPs typically come with a cut-off date (the latest date by which CPs must be fulfilled), after which either party may terminate the deal if the conditions remain unfulfilled.

- Some CPs may be waived by the parties, partially or fully, typically with Buyer’s consent, without preventing the deal from closing.

- Documentary evidence is typically required to demonstrate fulfilment.

Examples

- Shareholders’ / Directors’ approvals

- Regulatory approvals

- Third-party consents (e.g financiers, suppliers, etc.)

- Removal of encumbrances

- Settlement of major disputes

- Completion of internal restructuring

- Achievement of minimum profitability

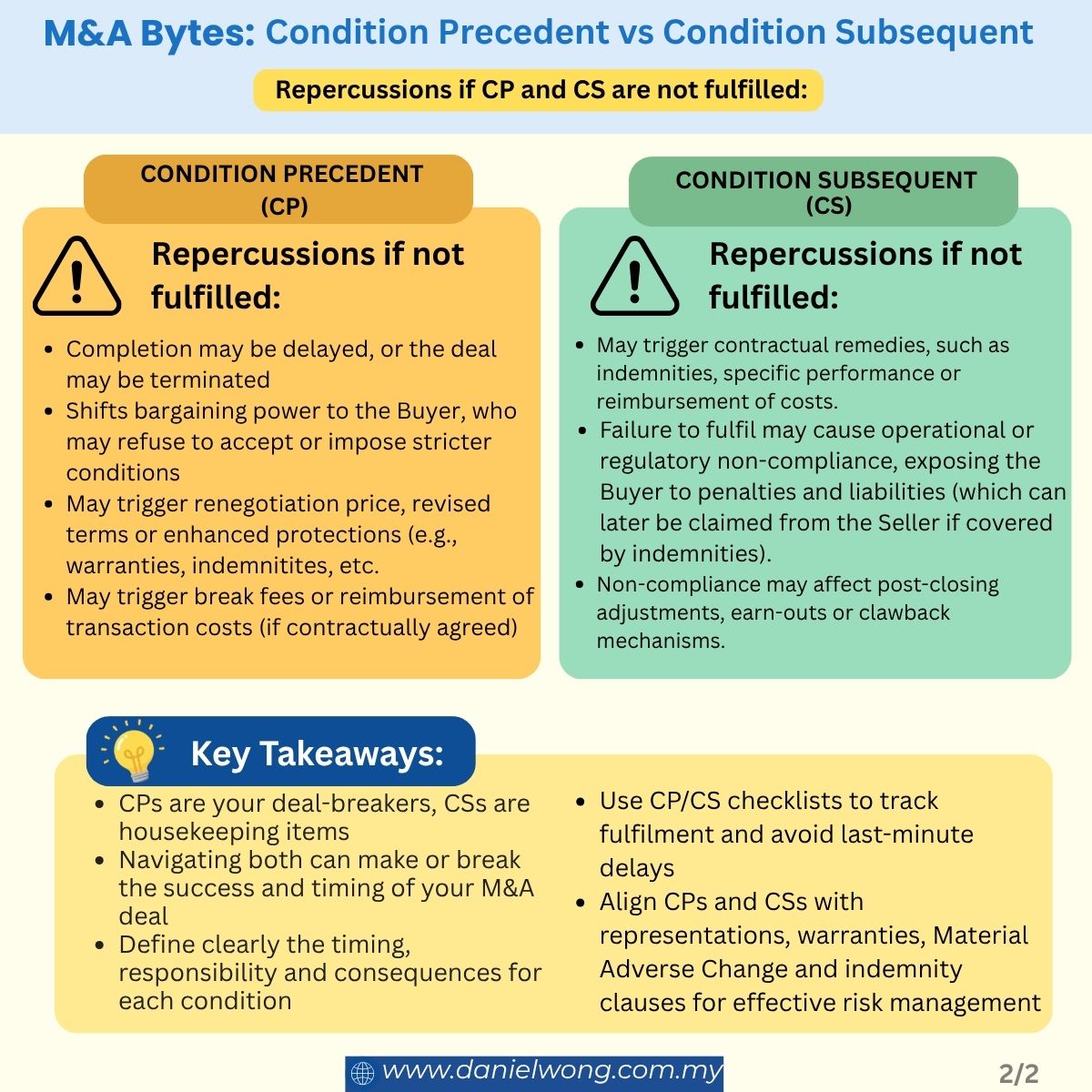

Repercussions if not fulfilled

- Completion may be delayed, or the deal may be terminated.

- Failure to fulfil CPs often shifts bargaining power to the Buyer, who may refuse to accept or impose stricter conditions.

- May trigger renegotiation of price, revised terms or enhanced protections (e.g. warranties, indemnities, etc.).

- In some cases, non-fulfilment may trigger break fees or reimbursement of transaction costs (if contractually agreed).

What are Conditions Subsequent?

Condition Subsequent

Conditions Subsequent (“CS“) are future, uncertain events that occur after the deal has closed and can cancel or undo the existing agreement if they fail to happen.In essence, CS:- Must be fulfilled after completion, treated as post-closing obligations.

- Typically covers less critical or administrative items that do not affect the deal’s closing.

- May include certain approvals or formalities that can only be completed once the Buyer becomes the new owner of the company.

- Similar to CPs, documentary evidence is typically required to indicate fulfilment.

Examples

- Updating and republishing privacy policies in both Bahasa Malaysia and English.

- Updating or reissuing employee handbooks.

- Stamping or re-stamping contracts.

- Transferring licences or permits that can only be applied post-completion.

- Carrying out agreed minor operational or IT integrations (e.g. system access updates, etc.)

Repercussions if not fulfilled

- May trigger contractual remedies, such as indemnities, specific performance or reimbursement of costs.

- Failure to fulfil may cause operational or regulatory non-compliance, exposing the Buyer to penalties and liabilities (which can later be claimed from the Seller if covered by indemnities).

- Non-compliance may affect post-closing adjustments, earn-outs or clawback mechanisms.

🔑 Key Takeaway:

- CPs are mostly your deal-breakers, and CSs are most likely your housekeeping items.

- Navigating CPs and CSs can make or break the success and timing of your M&A deal.

- Parties should clearly define the timing, responsibility and consequences for each condition.

- Use CP / CS checklists to track fulfilment and avoid last-minute delays.

- Align CPs and CSs with representations, warranties, MAC and indemnity clauses for effective risk management.

In Essence:

Disclaimer: The content of this article is intended for general informational purposes only and does not constitute formal legal advice.

Our Corporate team regularly advises local and international corporations on mergers and acquisitions (M&A), cross-border transactions, joint ventures, and corporate restructuring. We also provide comprehensive support for shareholders’ agreements and general commercial advisory to help businesses navigate the Malaysian regulatory landscape.

For legal assistance or further inquiries regarding your corporate matters, please feel free to contact us.

- July 15, 2026

ASICS Corporation has announced plans to separate its high-growth lifestyle brand Onitsuka Tiger into a standalone, wholly owned subsidiary, OT GROUP, with the reorganisation expected to take effect on 1 January 2027. Despite the separation, ASICS will remain the sole shareholder of OT GROUP, with the restructuring aimed at streamlining decision-making and strengthening Onitsuka Tiger’s global competitiveness.

From a strategic standpoint, the reorganisation reflects a growing trend among multinational groups to separate high-performing business units into dedicated entities, enabling greater operational autonomy while retaining ownership. Such carve-out structures can sharpen brand positioning, enhance management focus and provide greater strategic flexibility for future corporate actions. This can also be seen as part of a risk management strategy.

Taken together, these developments highlight how corporate restructurings can be as significant as traditional M&A transactions in unlocking value, improving governance, risk allocation and positioning businesses for long-term growth.

🌏 Follow us for monthly insights as our Global Deal Radar series highlights major M&A deals shaping industries worldwide.

Our Corporate team regularly advises local and international corporations on mergers and acquisitions (M&A), cross-border transactions, joint ventures, and corporate restructuring. We also provide comprehensive support for shareholders’ agreements and general commercial advisory to help businesses navigate the Malaysian regulatory landscape.

For legal assistance or further inquiries regarding your corporate matters, please feel free to contact us.

- June 30, 2026

You want a smooth exit – but gaps in approvals, consents, or corporate actions can derail the closing.

In every merger and acquisition (“M&A”) or transactional exercise, conditions precedent (“CPs”) act as critical checkpoints to ensure the business and the entity are in an acceptable state before completion. They help allocate risk and set expectations.

It is important to understand CPs and negotiate them well, as they directly affect deal certainty and timelines.

Why CPs exist and Common CPs

CPs exist to ensure that essential approvals, financial clean-ups, housekeeping matters, restructurings and third-party consents are completed before the buyer is locked in. It helps verify that the business is deliverable as promised.Common CPs include:- Regulatory Approvals: Licences and approvals

- Corporate Approvals: Board and shareholder resolutions from both sides

- Third-Party Consents: Landlord consent for tenancy transfer or termination, financing consents from financiers, key customer or vendor consents

- Financial Housekeeping: Settlement of shareholder or intercompany loans, removal of guarantees

- Operational CPs: Internal restructuring, transfer of employees, assignment or novation of key operational contracts

Practical Challenges & Impact on Deal Certainty

Practical Challenges:-

- Negotiating which CPs are truly necessary vs “nice to have”.

- Buyers often try to insert a long list of CPs to safeguard themselves from perceived risks. Sellers push back because every CP increases the risk that the deal does not close.

- The challenge lies in balancing legitimate concerns with the practical ability to deliver the CP within the transaction timeline.

- Determining who is responsible for satisfying each CP.

- Some CPs are clearly for the seller, while some are for the buyer. Some also require both parties’ cooperation.

- Setting a realistic cutoff date to satisfy the CPs.

- Regulatory approvals are often the longest and most unpredictable. If timelines are unrealistic, the transaction may drag on, lose momentum or face external market risks.

Why CPs affect Deal Certainty:-

- Too many CPs can lower deal certainty. This, in turn, would result in longer timelines and higher execution risks.

- Thus, well-tailored CPs would streamline completion and keep both parties aligned.

🔑 Key Takeaway:

CPs aren’t just formalities. They safeguard the transaction and ensure that the buyer gets the business they expect.

To be effective, CPs should always be:

- Clear: Leaves no room for multiple interpretations.

- Achievable: To be negotiated within a realistic timeframe.

- Necessary: Focusing only on conditions that materially impact the buyer’s risk.

In Essence:

Disclaimer: The content of this article is intended for general informational purposes only and does not constitute formal legal advice.

Our Corporate team regularly advises local and international corporations on mergers and acquisitions (M&A), cross-border transactions, joint ventures, and corporate restructuring. We also provide comprehensive support for shareholders’ agreements and general commercial advisory to help businesses navigate the Malaysian regulatory landscape.

For legal assistance or further inquiries regarding your corporate matters, please feel free to contact us.

- June 16, 2026

Berkshire Hathaway has announced its proposed acquisition of Taylor Morrison Home Corporation, one of the largest homebuilders in the United States, in an all-cash transaction valued at approximately US$8.5 billion. The deal marks the first major acquisition under Berkshire’s new Chief Executive Officer, Greg Abel, and reflects Berkshire’s continued commitment to the US housing market.

Beyond expanding Berkshire’s housing portfolio, the transaction is expected to complement its existing housing and building products businesses. Notably, Berkshire has indicated in its announcement that it intends to eventually unify its site-built homebuilding operations into a combined platform, signalling a strategic move towards greater scale and operational integration in the sector.

Taken together, this deal demonstrates how strategic acquisitions can be deployed to strengthen market position during cyclical downturns, while highlighting the role of long-term capital in driving consolidation within mature industries.

🌏 Follow us for monthly insights as our Global Deal Radar series highlights major M&A deals shaping industries worldwide.

Our Corporate team regularly advises local and international corporations on mergers and acquisitions (M&A), cross-border transactions, joint ventures, and corporate restructuring. We also provide comprehensive support for shareholders’ agreements and general commercial advisory to help businesses navigate the Malaysian regulatory landscape.

For legal assistance or further inquiries regarding your corporate matters, please feel free to contact us.

- June 4, 2026

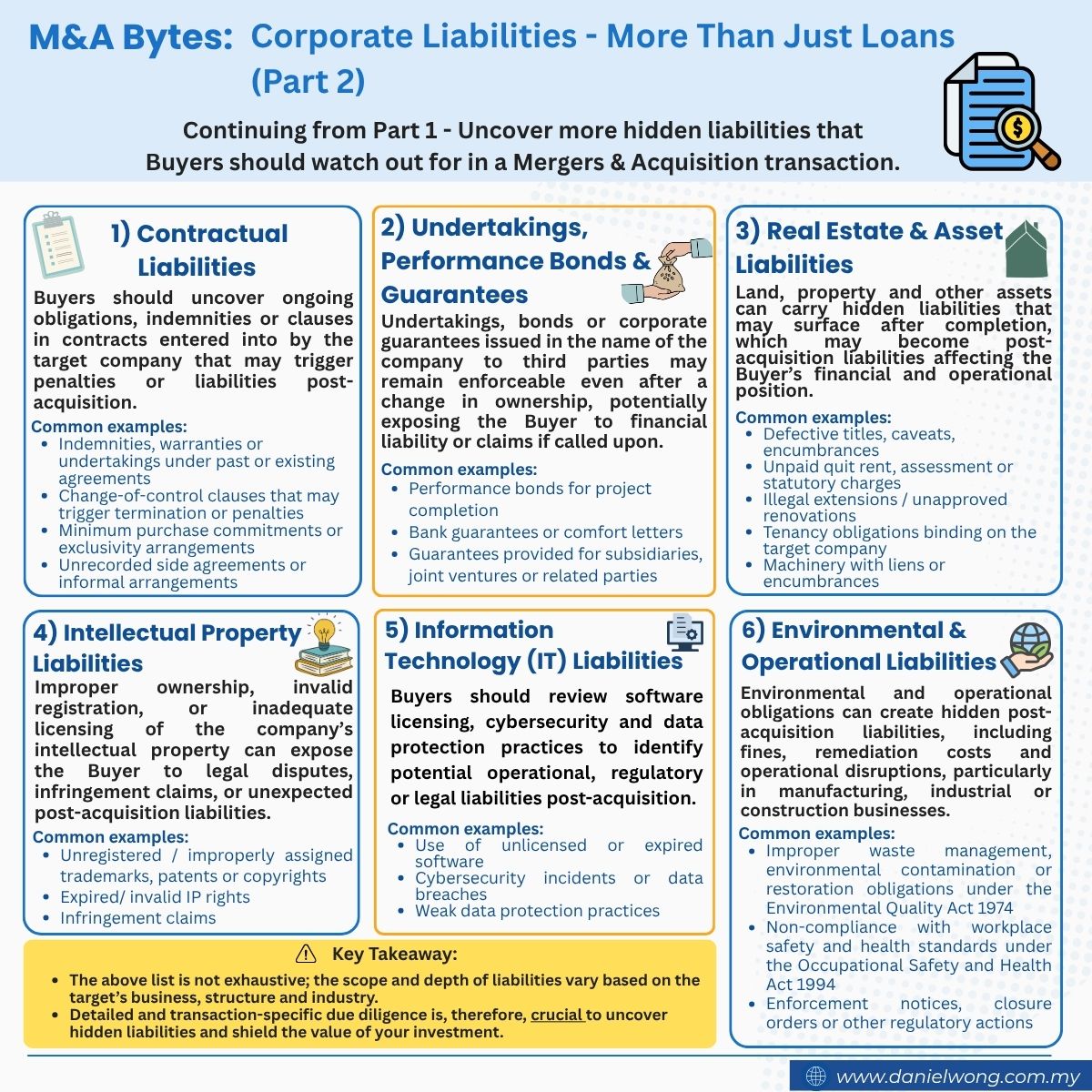

Would you still buy – or could you still sell – if the business you thought you knew had problems you didn’t even know existed?

Continuing from Part 1, let’s uncover more hidden liabilities that Buyers should watch out for in an M&A transaction.

Key Areas to Uncover:

(1) Contractual Liabilities

Buyers should uncover ongoing obligations, indemnities or clauses in contracts entered into by the target company that may trigger penalties or liabilities post-acquisition.Common examples:- Indemnities, warranties or undertakings under past or existing agreements

- Change-of-control clauses that may trigger termination or penalties

- Minimum purchase commitments or exclusivity arrangements

- Unrecorded side agreements or informal arrangements

(2) Undertakings, Performance Bonds & Guaranties

Undertakings, bonds or corporate guarantees issued in the name of the company to third parties may remain enforceable even after a change in ownership, potentially exposing the Buyer to financial liability or claims if called upon.

Common examples:

- Performance bonds for project completion

- Bank guarantees or comfort letters

- Guarantees provided for subsidiaries, joint ventures or related parties

(3) Real Estate & Asset Liabilities

Land, property and other assets can carry hidden liabilities that may surface after completion, which may become post-acquisition liabilities affecting the Buyer’s financial and operational position.

Common examples:

- Defective titles, caveats, encumbrances

- Unpaid quit rent, assessment or statutory charges

- Illegal extensions / unapproved renovations

- Tenancy obligations binding on the target company

- Machinery with liens or encumbrances

(4) Intellectual Property Liabilities

Improper ownership, invalid registration, or inadequate licensing of the company’s intellectual property can expose the Buyer to legal disputes, infringement claims, or unexpected post-acquisition liabilities.

Common examples:

- Unregistered or improperly assigned trademarks, patents or copyrights

- Expired or invalid IP rights

- Infringement claims

(5) Information Technology (IT) Liabilities

In today’s digital landscape, a company’s IT systems are generally crucial to its operations — but they can also be a hidden source of risk. Buyers should review software licensing, cybersecurity and data protection practices to identify potential operational, regulatory or legal liabilities post-acquisition.

Common examples:

- Use of unlicensed or expired software

- Cybersecurity incidents or data breaches

- Weak data protection practices

(6) Environmental & Operational Liabilities

Environmental and operational obligations can create hidden post-acquisition liabilities, including fines, remediation costs and operational disruptions, particularly in manufacturing, industrial or construction businesses.

Common examples:

- Improper waste management, environmental contamination or restoration obligations under the Environmental Quality Act 1974

- Non-compliance with workplace safety and health standards under Occupational Safety and Health Act 1994

- Enforcement notices, closure orders or other regulatory actions

🔑 Key Takeaway:

The above list is not exhaustive – the scope and depth of liabilities vary based on the target’s business, structure and industry.

A detailed and transaction-specific due diligence is therefore crucial to uncover hidden liabilities and shield the value of a buyer’s investment.

In Essence:

Disclaimer: The content of this article is intended for general informational purposes only and does not constitute formal legal advice.

Our Corporate team regularly advises local and international corporations on mergers and acquisitions (M&A), cross-border transactions, joint ventures, and corporate restructuring. We also provide comprehensive support for shareholders’ agreements and general commercial advisory to help businesses navigate the Malaysian regulatory landscape.

For legal assistance or further inquiries regarding your corporate matters, please feel free to contact us.

- May 19, 2026

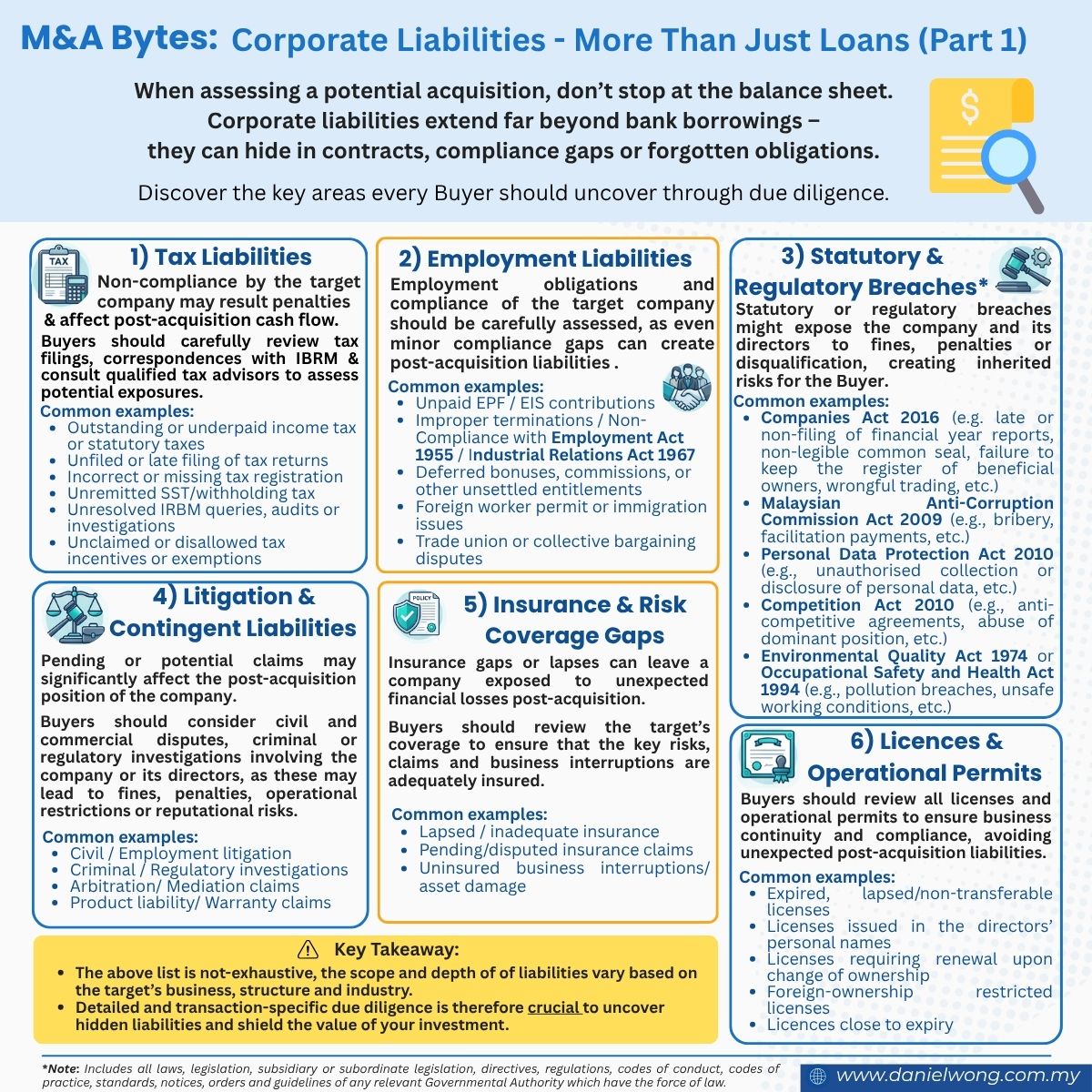

Would you still buy – or could you still sell – if the business you thought you knew had problems you didn’t even know existed?

When assessing a potential acquisition, don’t stop at the balance sheet. Corporate liabilities extend far beyond bank borrowings – they can hide in contracts, compliance gaps or forgotten obligations.

In Part 1 of Corporate Liabilities – More than Just Loans, discover the key areas every Buyer should uncover through due diligence.

Key Areas to Uncover:

(1) Tax Liabilities

The non-compliance with tax obligations by the target company may result in penalties and affect post-acquisition cash flow.Buyers should carefully review the target company’s tax filings and correspondence with the Inland Revenue Board of Malaysia (“IRBM”), and consult qualified tax advisors to assess potential exposures.Common examples:- Outstanding or underpaid income tax or other statutory taxes

- Unfiled or late filing of tax return

- Incorrect or missing tax registration

- Unremitted SST/ withholding tax

- Unresolved IBRM queries, audits or investigations

- Unclaimed or disallowed tax incentives or exemptions

(2) Employment Liabilities

The target company’s employment obligations and compliance should be carefully assessed, as even minor compliance gaps can create post-acquisition liabilities.

Common scenarios include:

- Unpaid EPF, SOCSO or EIS contributions

- Improper terminations or non-compliance with the Employment Act 1955 / Industrial Relations Act 1967

- Deferred bonuses, commissions or other unsettled entitlements

- Foreign worker permit or immigration issues

- Trade union or collective bargaining disputes

(3) Statutory & Regulatory Breaches*

Statutory or regulatory breaches might expose the company and its directors to fines, penalties or even disqualification, creating inherited risks for the Buyer.

Common examples:

- Companies Act 2016 (e.g. late or non-filing of financial year reports, non-legible common seal, failure to keep the register of beneficial owners, fraudulent or wrongful trading, etc.)

- Malaysian Anti-Corruption Commission Act 2009 (e.g. bribery, facilitation payments, failure to maintain anti-corruption policies, etc.)

- Personal Data Protection Act 2010 (e.g., unauthorised collection or disclosure of personal data,

- Competition Act 2010 (e.g. anti-competitive agreements, abuse of dominant position, etc.)

- Environmental Quality Act 1974 or Occupational Safety and Health Act 1994 (e.g. pollution breaches, unsafe working conditions, failure to obtain environmental approvals, etc.)

*Note: Includes all laws, legislation, subsidiary or subordinate legislation, directives, regulations, codes of conduct, codes of practice, standards, notices, orders and guidelines of any relevant Governmental Authority which have the force of law.

(4) Litigation & Contingent Liabilities

Pending or potential claims may significantly affect the company’s post-acquisition position.

Buyers should consider not only civil and commercial disputes, but also any criminal or regulatory investigations involving the company or its directors, as these may lead to fines, penalties, operational restrictions or reputational risks.

Common examples:

- Civil or employment litigation

- Criminal or regulatory investigations

- Arbitration or mediation claims

- Product liability or warranty claims

(5) Insurance & Risk Coverage Gaps

Insurance gaps or lapses can leave a company exposed to unexpected financial losses post-acquisition.

Buyers should carefully review the target’s coverage to ensure that the key risks, claims and business interruptions are adequately insured.

Common examples:

- Lapsed or inadequate insurance

- Pending or disputed insurance claims

- Uninsured business interruptions or asset damage.

(6) Licences & Operational Permits

Buyers should review all licences and operational permits to ensure business continuity and compliance. This is to avoid unexpected post-acquisition liabilities.

Common examples:

- Expired, lapsed or non-transferable licences

- Licences issued in the directors’ personal names

- Licences requiring renewal upon change of ownership

- Foreign-ownership restricted licences

- Licences close to expiry

🔑 Key Takeaway:

The above list is not exhaustive – the scope and depth of liabilities vary based on the target’s business, structure and industry.

A detailed and transaction-specific due diligence is therefore crucial to uncover hidden liabilities and shield the value of a buyer’s investment.

In Essence:

Disclaimer: The content of this article is intended for general informational purposes only and does not constitute formal legal advice.

Our Corporate team regularly advises local and international corporations on mergers and acquisitions (M&A), cross-border transactions, joint ventures, and corporate restructuring. We also provide comprehensive support for shareholders’ agreements and general commercial advisory to help businesses navigate the Malaysian regulatory landscape.

For legal assistance or further inquiries regarding your corporate matters, please feel free to contact us.

- May 5, 2026

The Estée Lauder Companies Inc is reportedly exploring strategic M&A opportunities involving Puig, the Spanish beauty and fashion group, as part of its broader portfolio optimisation and growth strategy. While details of a full acquisition remain speculative, Estée Lauder has recently acquired a stake in luxury skincare brand 111SKIN, which is backed by Puig – signalling potential alignment between the two groups in the premium beauty segment.

From a strategic standpoint, this potential transaction would reflect a broader trend in the global beauty industry, where established industry players are pursuing partnerships and acquisitions to strengthen their presence in luxury and niche segments. A combination of Estée Lauder’s global distribution capabilities with Puig’s strong brand portfolio could create a more diversified and competitive player in the industry.

These developments highlight the increasing role of strategic investments and minority stakes as precursors to larger M&A deals, while underscoring the execution and integration considerations in cross-border consumer deals.

🌏 Follow us for monthly insights as our Global Deal Radar series highlights major M&A deals shaping industries worldwide.

Our Corporate team regularly advises local and international corporations on mergers and acquisitions (M&A), cross-border transactions, joint ventures, and corporate restructuring. We also provide comprehensive support for shareholders’ agreements and general commercial advisory to help businesses navigate the Malaysian regulatory landscape.

For legal assistance or further inquiries regarding your corporate matters, please feel free to contact us.

- April 21, 2026

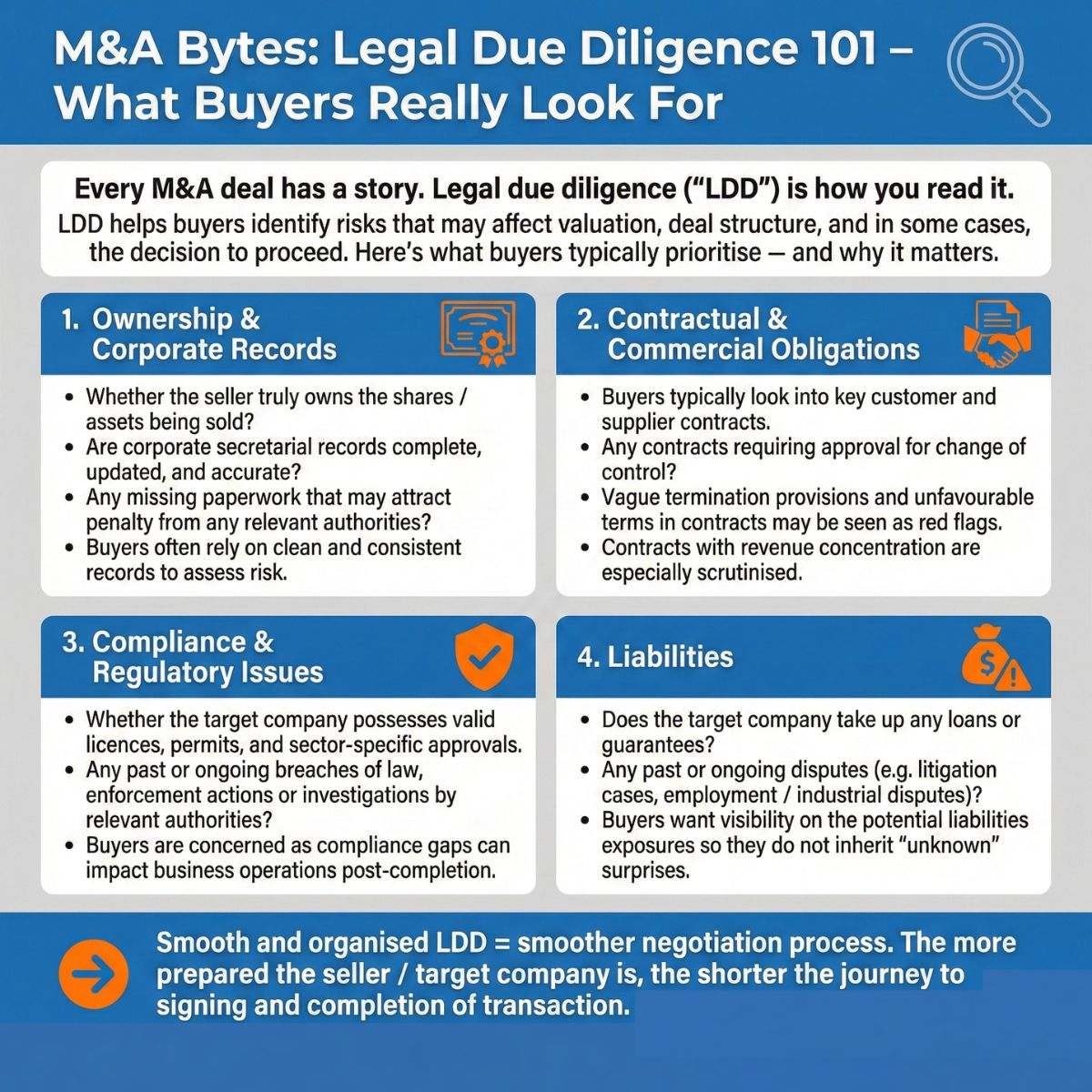

Every M&A deal has a story. Legal due diligence (“LDD”) is how you read it.

LDD helps buyers identify risks that may affect valuation, deal structure, and in some cases, the decision to proceed with the transaction.

Here’s what buyers typically prioritise – and why it matters for both sides.

1. Ownership & Corporate Records

- Whether the seller truly owns the shares/assets being sold?

- Are corporate secretarial records complete, updated, and accurate?

- Any missing paperwork that may attract a penalty from any relevant authorities?

- Buyers often rely on clean and consistent records to assess risk.

2. Contractual & Commercial Obligations

- Buyers typically look into key customer and supplier contracts.

- Any contracts requiring approval for a change of control?

- Vague termination provisions and unfavourable terms in contracts may be seen as red flags.

- Contracts with revenue concentration are especially scrutinised.

3. Compliance & Regulatory Issues

- Whether the target company possesses valid licences, permits, and sector-specific approvals.

- Any past or ongoing breaches of law, enforcement actions or investigations by relevant authorities?

- Buyers are concerned as compliance gaps can impact business operations post-completion.

4. Liabilities

- Does the target company take out any loans or provide guarantees?

- Any past or ongoing disputes (e.g. litigation cases, employment / industrial disputes)?

- Buyers want visibility into the potential liabilities and exposures so they do not inherit “unknown” surprises.

🔑 Key Takeaway:

Smooth and organised LDD equates to a smoother negotiation process.

The more prepared the seller/target company is, the shorter the journey to signing and completion of the transaction.

In Essence:

Disclaimer: The content of this article is intended for general informational purposes only and does not constitute formal legal advice.

Our Corporate team regularly advises local and international corporations on mergers and acquisitions (M&A), cross-border transactions, joint ventures, and corporate restructuring. We also provide comprehensive support for shareholders’ agreements and general commercial advisory to help businesses navigate the Malaysian regulatory landscape.

For legal assistance or further inquiries regarding your corporate matters, please feel free to contact us.

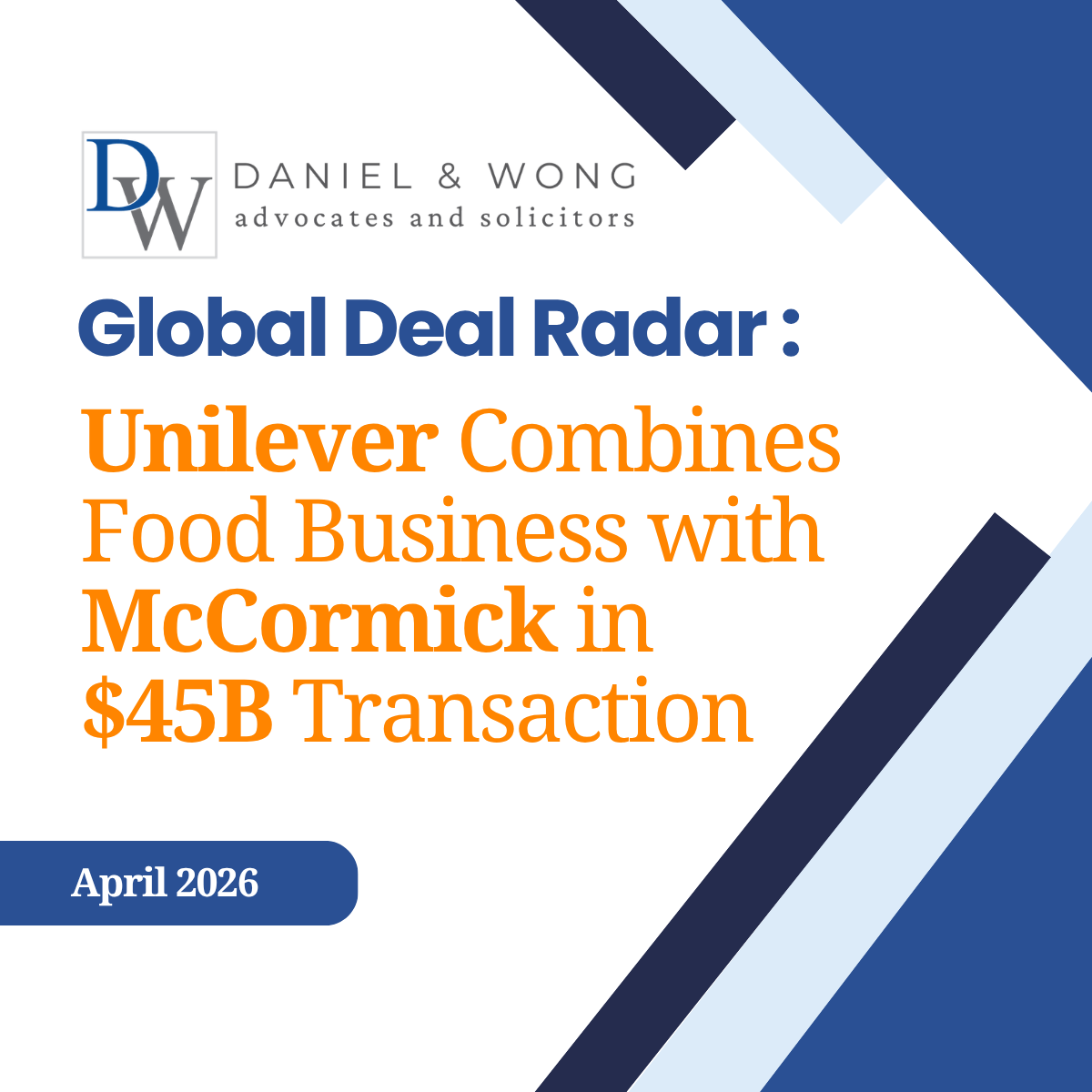

- April 7, 2026

Unilever and McCormick & Company (“McCormick“) have announced an agreement to combine Unilever Foods business with McCormick, in a transaction valuing the business at approximately US$44.8 billion. The proposed transaction will see Unilever and its shareholders receive a majority equity stake in the combined entity, forming a global flavour-focused company with significant scale across retail and food service channels.

Structurally, the transaction is expected to be implemented through a Reverse Morris Trust arrangement, enabling a tax-free separation of Unilever Foods business for US federal income tax purposes while combining it with McCormick’s existing operations. This reflects a growing trend of strategic carve-outs and business separations in large-scale M&A, particularly where conglomerates seek to enhance portfolio focus in a tax-efficient manner.

Taken together, the proposed combination highlights how complex deal structuring and tax considerations remain central to executing large-scale transactions.

🌏 Follow us for monthly insights into significant M&A deals around the world.

Our Corporate team regularly advises local and international corporations on mergers and acquisitions (M&A), cross-border transactions, joint ventures, and corporate restructuring. We also provide comprehensive support for shareholders’ agreements and general commercial advisory to help businesses navigate the Malaysian regulatory landscape.

For legal assistance or further inquiries regarding your corporate matters, please feel free to contact us.

- March 24, 2026

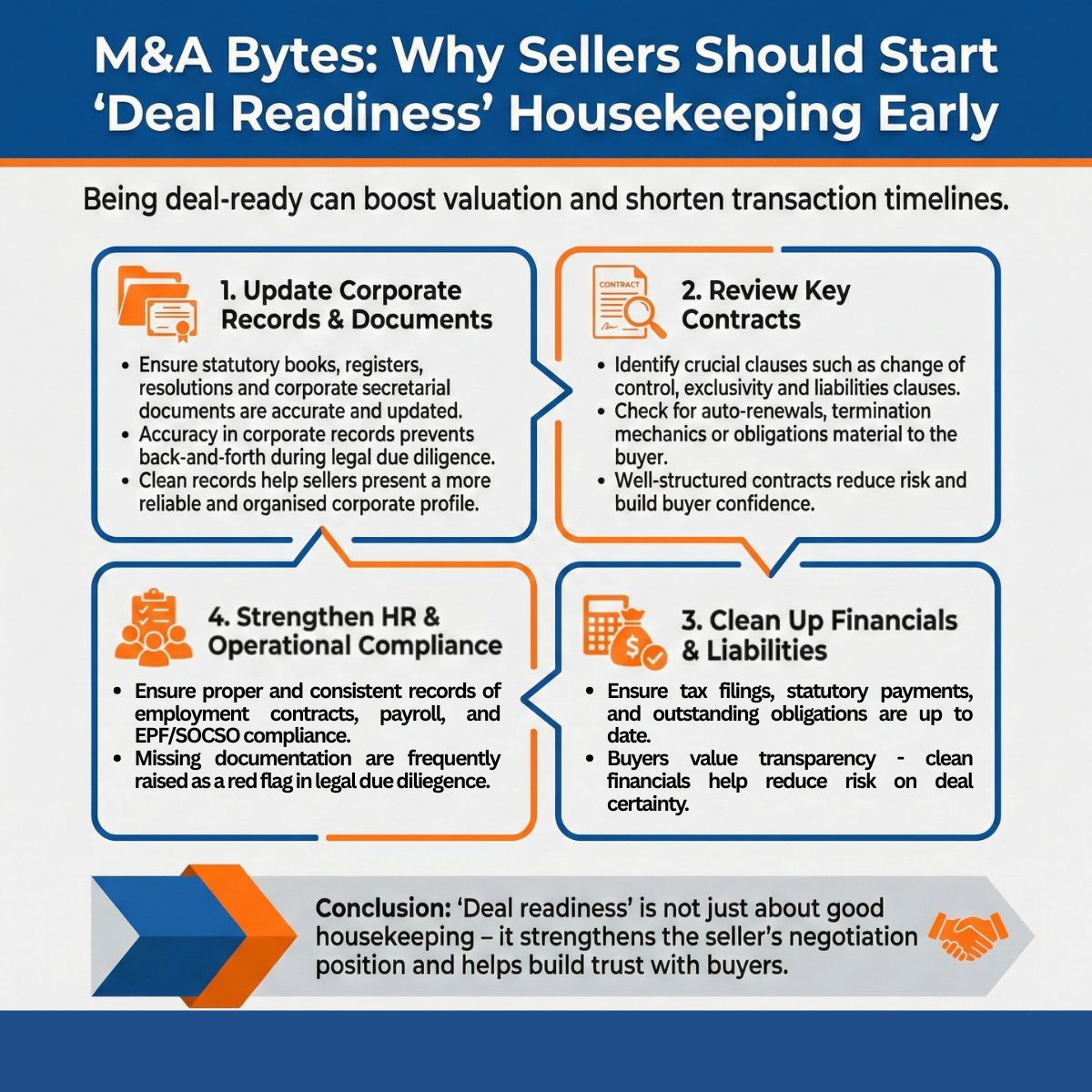

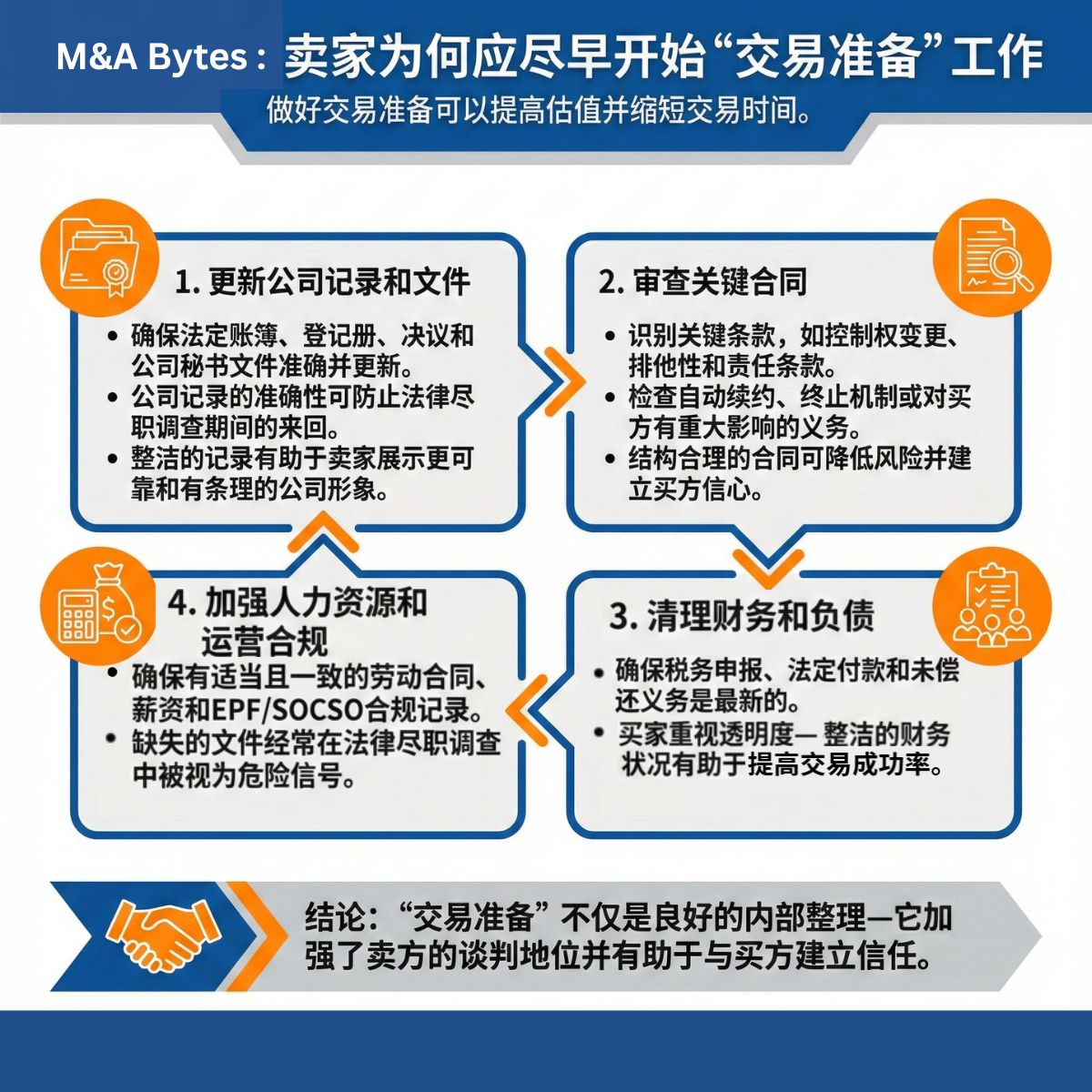

What if being deal-ready, with your documents and compliance in order, could increase your valuation and speed up your sale?

In this M&A Byte, it explains the early seller preparations, which typically include:

- Clean and updated corporate records

- Well-reviewed contracts with key risk clauses identified

- Clear financials and managed liabilities

- Consistent HR and operational compliance

Strong housekeeping isn’t administrative hygiene; it is a commercial advantage.

Here’s how sellers can prepare.

1. Update Corporate Records & Documents

- Ensure statutory books, registers, resolutions and corporate secretarial documents are accurate and updated.

- Accuracy in corporate records prevents back-and-forth during legal due diligence.

- Clean records help sellers present a more reliable and organised corporate profile.

2. Review Key Contracts

- Identify crucial clauses such as change of control, exclusivity and liabilities clauses.

- Check for auto-renewals, termination mechanics or obligations material to the buyer.

- Well-structured contracts reduce risk and build buyer confidence.

3. Clean Up Financials & Liabilities

- Ensure tax filings, statutory payments, and outstanding obligations are up to date.

- Buyers value transparency – clean financials help reduce risk on deal certainty.

4. Strengthen HR & Operational Compliance

- Ensure proper and consistent records of employment contracts, payroll, and EPF/SOCSO compliance.

- Missing documentation is frequently raised as a red flag in legal due diligence.

🔑 Key Takeaway:

“Deal readiness” is not just about good housekeeping – it strengthens the seller’s negotiation position and helps build trust with buyers.

In Essence:

Disclaimer: The content of this article is intended for general informational purposes only and does not constitute formal legal advice.

Our Corporate team regularly advises local and international corporations on mergers and acquisitions (M&A), cross-border transactions, joint ventures, and corporate restructuring. We also provide comprehensive support for shareholders’ agreements and general commercial advisory to help businesses navigate the Malaysian regulatory landscape.

For legal assistance or further inquiries regarding your corporate matters, please feel free to contact us.