Mergers & Acquisitions

- April 21, 2026

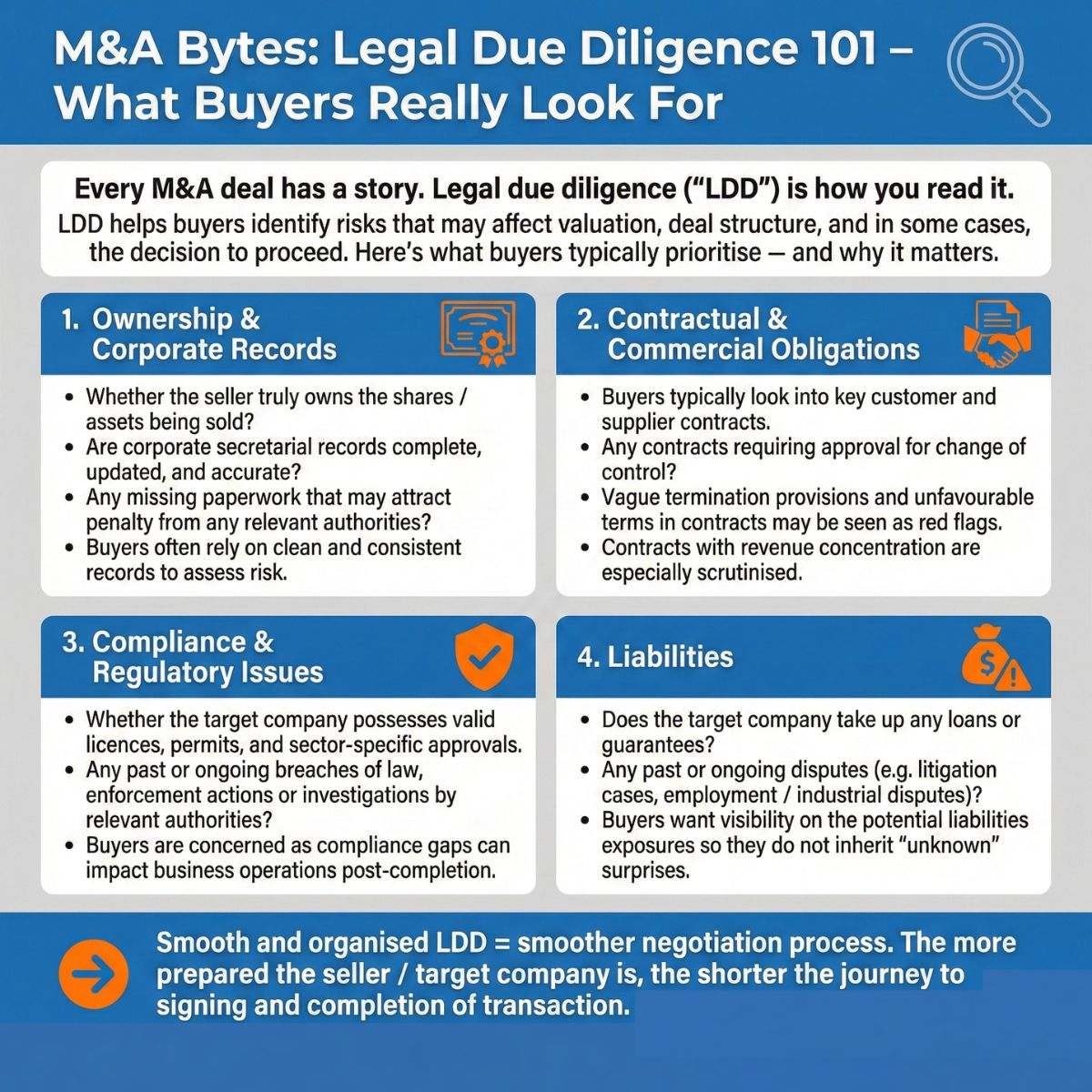

Every M&A deal has a story. Legal due diligence (“LDD”) is how you read it.

LDD helps buyers identify risks that may affect valuation, deal structure, and in some cases, the decision to proceed with the transaction.

Here’s what buyers typically prioritise – and why it matters for both sides.

1. Ownership & Corporate Records

- Whether the seller truly owns the shares/assets being sold?

- Are corporate secretarial records complete, updated, and accurate?

- Any missing paperwork that may attract a penalty from any relevant authorities?

- Buyers often rely on clean and consistent records to assess risk.

2. Contractual & Commercial Obligations

- Buyers typically look into key customer and supplier contracts.

- Any contracts requiring approval for a change of control?

- Vague termination provisions and unfavourable terms in contracts may be seen as red flags.

- Contracts with revenue concentration are especially scrutinised.

3. Compliance & Regulatory Issues

- Whether the target company possesses valid licences, permits, and sector-specific approvals.

- Any past or ongoing breaches of law, enforcement actions or investigations by relevant authorities?

- Buyers are concerned as compliance gaps can impact business operations post-completion.

4. Liabilities

- Does the target company take out any loans or provide guarantees?

- Any past or ongoing disputes (e.g. litigation cases, employment / industrial disputes)?

- Buyers want visibility into the potential liabilities and exposures so they do not inherit “unknown” surprises.

🔑 Key Takeaway:

Smooth and organised LDD equates to a smoother negotiation process.

The more prepared the seller/target company is, the shorter the journey to signing and completion of the transaction.

In Essence:

Disclaimer: The content of this article is intended for general informational purposes only and does not constitute formal legal advice.

Our Corporate team regularly advises local and international corporations on mergers and acquisitions (M&A), cross-border transactions, joint ventures, and corporate restructuring. We also provide comprehensive support for shareholders’ agreements and general commercial advisory to help businesses navigate the Malaysian regulatory landscape.

For legal assistance or further inquiries regarding your corporate matters, please feel free to contact us.

- April 7, 2026

Unilever and McCormick & Company (“McCormick“) have announced an agreement to combine Unilever Foods business with McCormick, in a transaction valuing the business at approximately US$44.8 billion. The proposed transaction will see Unilever and its shareholders receive a majority equity stake in the combined entity, forming a global flavour-focused company with significant scale across retail and food service channels.

Structurally, the transaction is expected to be implemented through a Reverse Morris Trust arrangement, enabling a tax-free separation of Unilever Foods business for US federal income tax purposes while combining it with McCormick’s existing operations. This reflects a growing trend of strategic carve-outs and business separations in large-scale M&A, particularly where conglomerates seek to enhance portfolio focus in a tax-efficient manner.

Taken together, the proposed combination highlights how complex deal structuring and tax considerations remain central to executing large-scale transactions.

🌏 Follow us for monthly insights into significant M&A deals around the world.

Our Corporate team regularly advises local and international corporations on mergers and acquisitions (M&A), cross-border transactions, joint ventures, and corporate restructuring. We also provide comprehensive support for shareholders’ agreements and general commercial advisory to help businesses navigate the Malaysian regulatory landscape.

For legal assistance or further inquiries regarding your corporate matters, please feel free to contact us.

- March 24, 2026

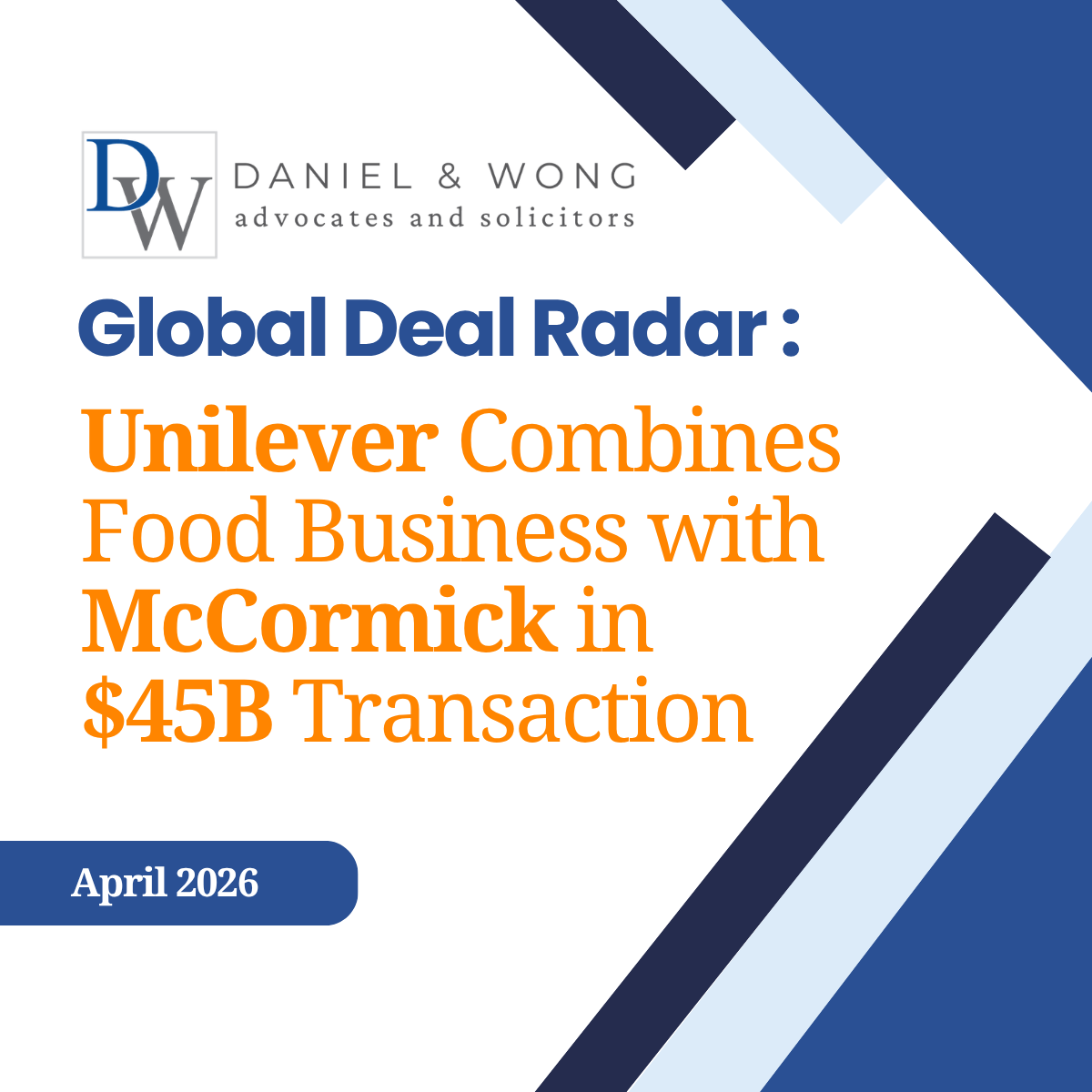

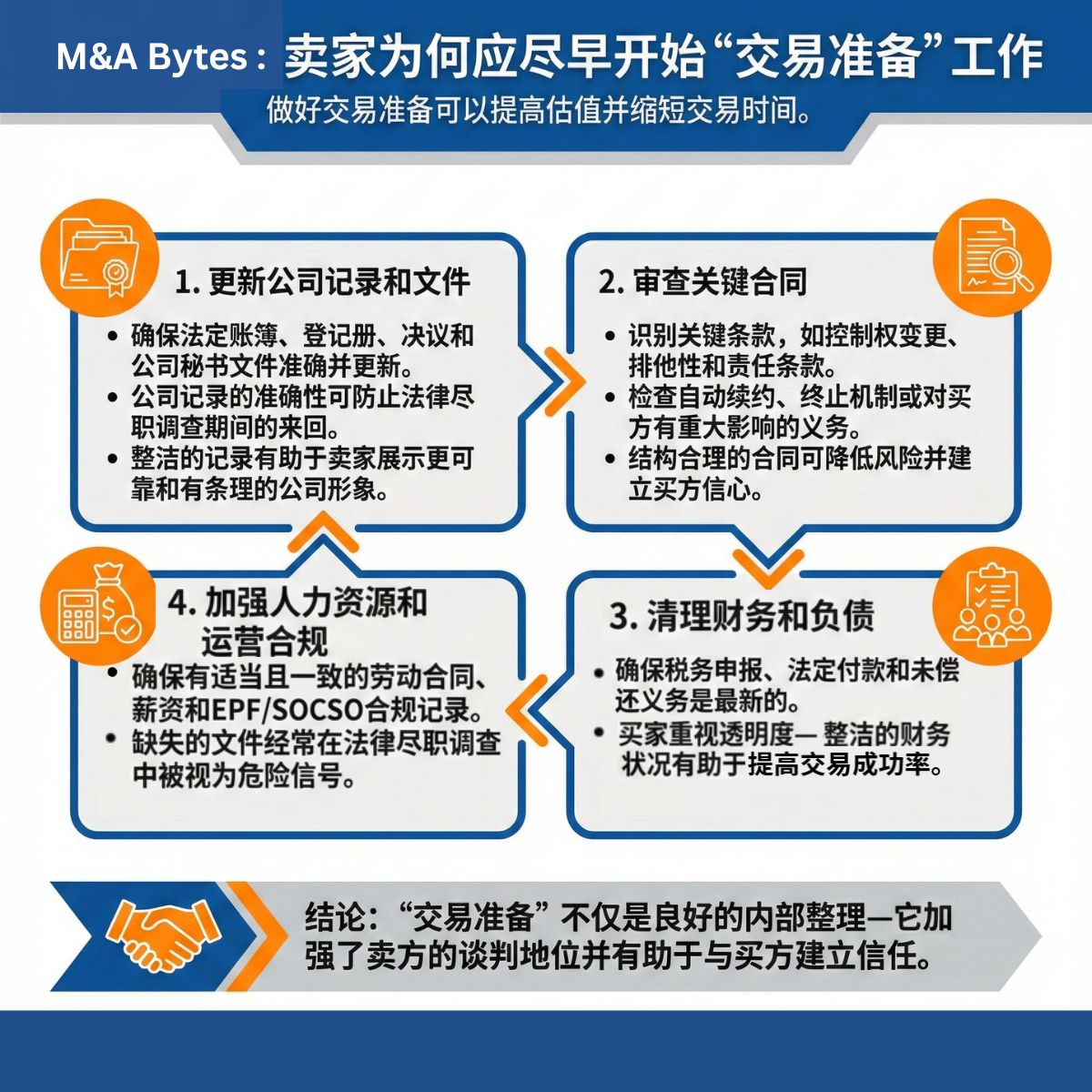

What if being deal-ready, with your documents and compliance in order, could increase your valuation and speed up your sale?

In this M&A Byte, it explains the early seller preparations, which typically include:

- Clean and updated corporate records

- Well-reviewed contracts with key risk clauses identified

- Clear financials and managed liabilities

- Consistent HR and operational compliance

Strong housekeeping isn’t administrative hygiene; it is a commercial advantage.

Here’s how sellers can prepare.

1. Update Corporate Records & Documents

- Ensure statutory books, registers, resolutions and corporate secretarial documents are accurate and updated.

- Accuracy in corporate records prevents back-and-forth during legal due diligence.

- Clean records help sellers present a more reliable and organised corporate profile.

2. Review Key Contracts

- Identify crucial clauses such as change of control, exclusivity and liabilities clauses.

- Check for auto-renewals, termination mechanics or obligations material to the buyer.

- Well-structured contracts reduce risk and build buyer confidence.

3. Clean Up Financials & Liabilities

- Ensure tax filings, statutory payments, and outstanding obligations are up to date.

- Buyers value transparency – clean financials help reduce risk on deal certainty.

4. Strengthen HR & Operational Compliance

- Ensure proper and consistent records of employment contracts, payroll, and EPF/SOCSO compliance.

- Missing documentation is frequently raised as a red flag in legal due diligence.

🔑 Key Takeaway:

“Deal readiness” is not just about good housekeeping – it strengthens the seller’s negotiation position and helps build trust with buyers.

In Essence:

Disclaimer: The content of this article is intended for general informational purposes only and does not constitute formal legal advice.

Our Corporate team regularly advises local and international corporations on mergers and acquisitions (M&A), cross-border transactions, joint ventures, and corporate restructuring. We also provide comprehensive support for shareholders’ agreements and general commercial advisory to help businesses navigate the Malaysian regulatory landscape.

For legal assistance or further inquiries regarding your corporate matters, please feel free to contact us.

- March 10, 2026

Luckin Coffee, China’s largest coffee chain, through its controlling shareholder Centurium Capital, is reportedly set to acquire the global café operations of Blue Bottle Coffee from Nestlé, valued at under US$400 million. If completed, the deal would combine Luckin’s technology-driven, high-volume coffee model with Blue Bottle’s premium specialty coffee brand and established international retail presence.

The proposed transaction also reflects a broader trend in consumer-sector M&A, where high-growth brands pursue acquisitions of established premium labels to diversify their brand portfolio and tap into new consumer segments. It also highlights how cross-border acquisitions continue to play a key role in global brand expansion, particularly in competitive consumer markets, such as specialty coffee.

🌏 Follow us for monthly insights into significant M&A deals around the world.

Our Corporate team regularly advises local and international corporations on mergers and acquisitions (M&A), cross-border transactions, joint ventures, and corporate restructuring. We also provide comprehensive support for shareholders’ agreements and general commercial advisory to help businesses navigate the Malaysian regulatory landscape.

For legal assistance or further inquiries regarding your corporate matters, please feel free to contact us.

- February 24, 2026

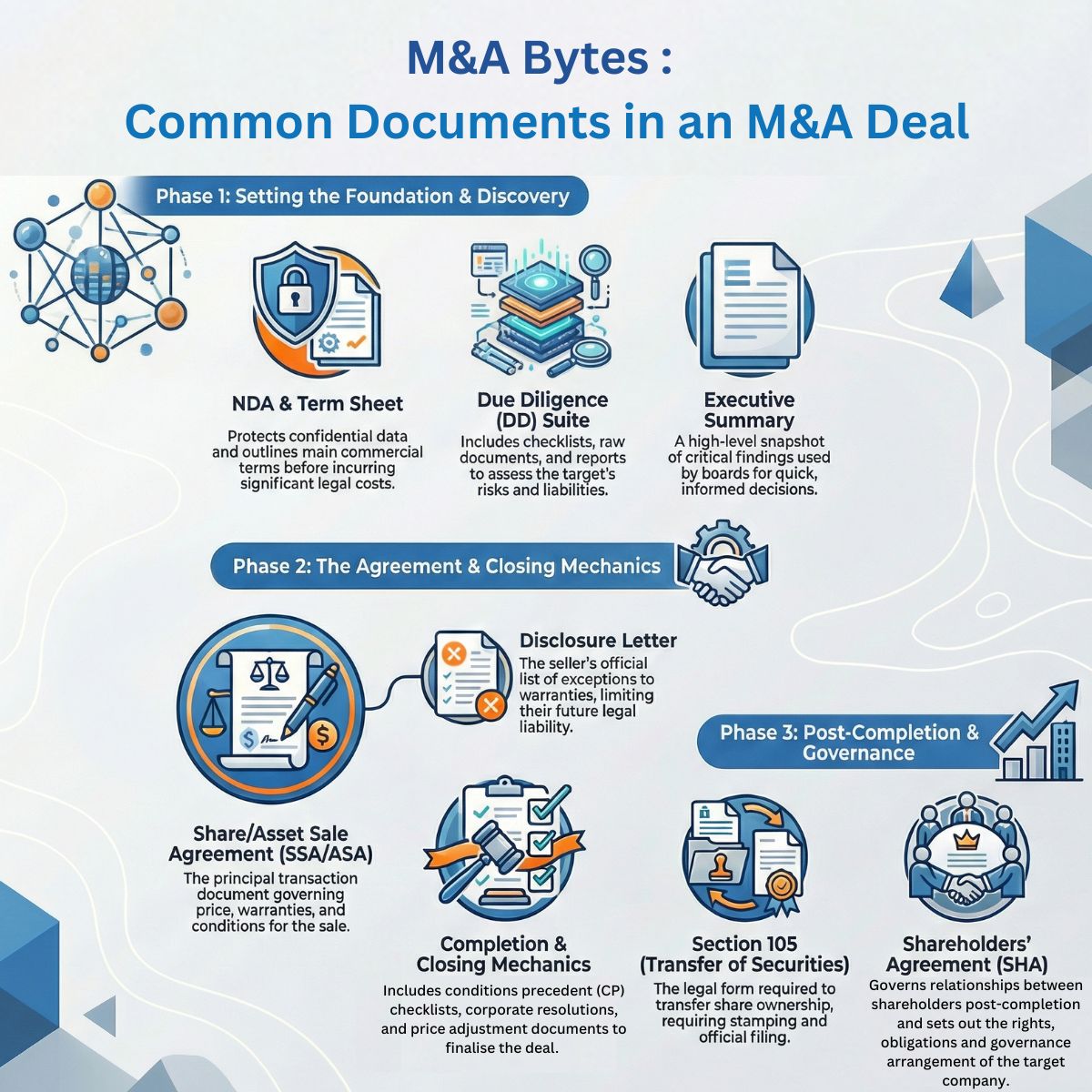

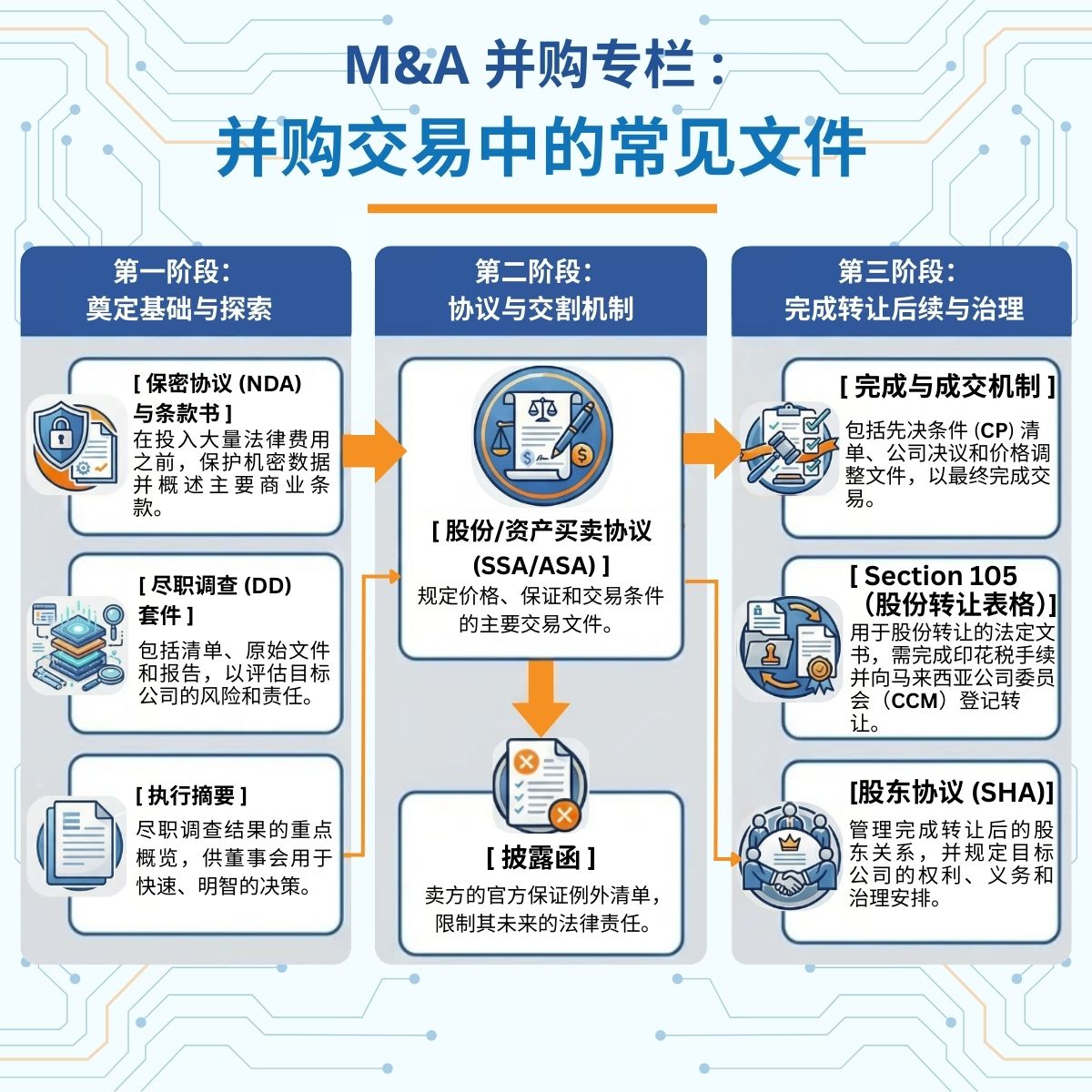

Behind every M&A transaction lies a stack of documents, each with a purpose.

Whether you are the vendor, buyer, solicitor or part of the target company’s management, understanding the role of each document is crucial.

This M&A Byte maps out:

- The core documents in a typical deal

- When they appear in the transaction lifecycle

- Why each one matter

Phase 1: Setting the Foundation

Document Function Non-Disclosure Agreement (NDA) - Signed before confidential information is shared for due diligence, typically after preliminary discussions or upon signing a Term Sheet.

- Prevents the Buyer (and its advisors/solicitors) from using the information for purposes other than the transaction.

- Protects confidential and high-level information shared by the Seller

- Can be mutual if both parties disclose sensitive information

Term Sheet / Letter of Intent (LOI) - Sets out the main commercial terms (e.g. price, structure, timeline, exclusivity).

- Provides a framework for negotiation and drafting of the Share Sale Agreement (“SSA”) or Asset Sale Agreement (“ASA”).

- While usually non-binding, certain clauses (e.g. exclusivity, confidentiality, break-up fees, etc.) can be binding.

- Helps both parties confirm alignment on key points before incurring further costs.

Due Diligence Checklist / Questionnaire - Prepared by the Buyer’s solicitors to request key documents and information about the target company from the S

- Forms the foundation for the due diligence process.

Due Diligence Documents - Reviewed by Buyer’s solicitors to: –

- inspect the target company’s background and

- assess potential risks or liabilities.

- E.g.:

- Corporate records (company secretarial forms)

- Material and operational contracts

- Employment documents

- Regulatory and litigation records

- Financial statements

- Tax filings

Phase 2: The Discovery & Core Agreements

Document Function List of Outstanding Issues/ Documents - After the initial Due Diligence Documents are provided for review, some items may be incomplete or require clarification.

- These tracks follow-up questions and requests for missing or incomplete documents.

- It maintains a clear record of what was requested, received and still pending.

Due Diligence Report - A report detailing the Buyer’s review of the Seller’s business.

- Includes findings on corporate, legal, operational and regulatory matters of the target company.

- Identifies risks, liabilities and potential deal issues.

- Highlights gaps, inconsistencies, or red flags in documentation.

- Provides the foundation for negotiation and adjustments to the terms in SSA/ASA.

Executive Summary - Condensed and high-level version of the Due Diligence Report.

- Highlights the critical findings and key risks.

- Used by senior management or boards to make informed decisions quickly.

Share Sale Agreement (“SSA”) / Asset Sale Agreement (“ASA”)

- The main transaction document, which sets out the detailed terms of the sale.

- Covers purchase price, representations and warranties, conditions precedent and completion deliverables.

Phase 3: Completion & Closing Mechanics

Document Function Conditions Precedent (“CP”) / Completion Checklists

- For both Seller and Buyer to track fulfilment of CP / Completion Deliverables.

Disclosure Letter - Prepared by the seller to disclose exceptions to the warranties given in the SSA/ASA.

- Helps limit the seller’s post-completion liability.

Resolutions - Formal approvals by directors and shareholders to authorise the deal and any other matters contemplated for the transaction.

- Without proper resolutions, the transaction may be rendered invalid or unenforceable.

Completion Accounts / Purchase Price Adjustment Documents

- Prepared to calculate adjustments to the final purchase price based on the actual financial position of the company at completion.

Phase 4: Post- Completion

Document Function Section 105 (Form of Transfer of Securities) - The legal transfer of share ownership from the Seller to the Buyer.

- Executed by both the Seller (as a transferor) and the Buyer (as a transferee).

- For the enforceability, the form needs to be:-

- stamped and filed with the Companies Commission of Malaysia, and

- reflected in the company’s Register of Members.

Shareholders’ Agreement (SHA) - Governs relationships between the company shareholders after completion.

- Sets out rights, obligations and governance arrangements of the target company.

🔑 Key Takeaway:

Every M&A deal is built on a suite of documents, each shaping the deal, defining risks and guiding decisions.

Understanding the purpose and interplay of these documents is essential for smooth execution, effective risk management and informed decision-making.

In Essence:

Disclaimer: The content of this article is intended for general informational purposes only and does not constitute formal legal advice.

Our Corporate team regularly advises local and international corporations on mergers and acquisitions (M&A), cross-border transactions, joint ventures, and corporate restructuring. We also provide comprehensive support for shareholders’ agreements and general commercial advisory to help businesses navigate the Malaysian regulatory landscape.

For legal assistance or further inquiries regarding your corporate matters, please feel free to contact us.

- February 12, 2026

We are pleased to have acted for the Purchaser in the acquisition of freehold industrial land located in Bandar Sri Sendayan, Negeri Sembilan.

The conditional sale and purchase agreement was entered into on 27 January 2026 with Sapura Machining Corporation Sdn Bhd, a wholly owned subsidiary of Sapura Industrial Berhad, for the acquisition of approximately 35,332 square metres of land at a total consideration of RM24.72 million.

🔗Official announcements on Bursa Malaysia:

Our Corporate team regularly advises local and international corporations on mergers and acquisitions (M&A), cross-border transactions, joint ventures, and corporate restructuring. We also provide comprehensive support for shareholders’ agreements and general commercial advisory to help businesses navigate the Malaysian regulatory landscape.

For legal assistance or further inquiries regarding your corporate matters, please feel free to contact us.

- January 27, 2026

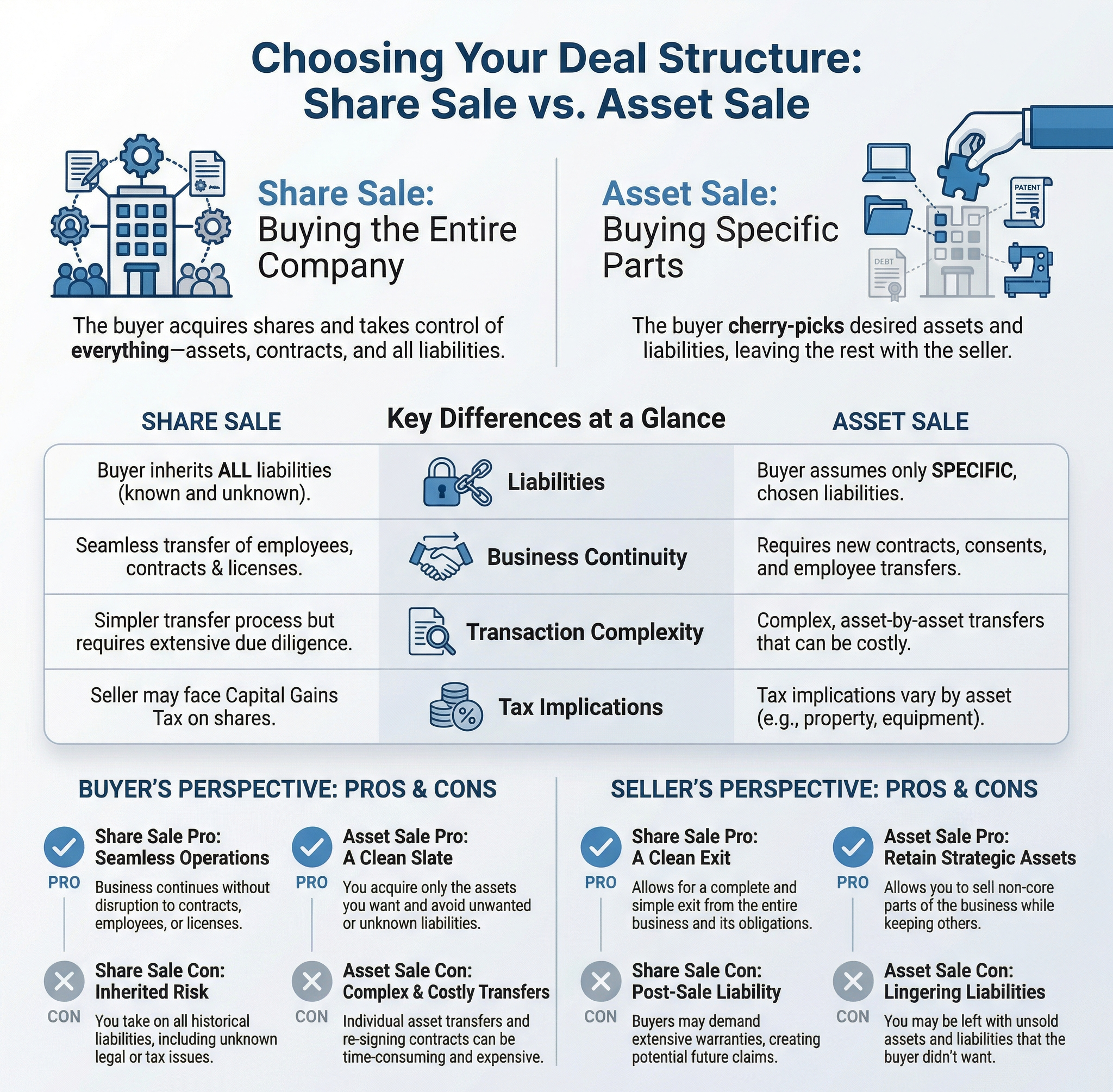

Are you buying the company or just what’s inside it? One decision. Major Consequences.

Every business acquisition starts with a critical question: Are you buying the company, or just the assets that matter to you?

- In a Share Sale, you acquire shares in the company — this may be 100% of the shares (full control) or a partial share sale. In either case, you take on the company’s assets, liabilities, contracts and its full corporate history.

- In an Asset Sale, you selectively acquire only the assets and operations you want, leaving the rest with the Seller.

Key Differences between Share Sale & Asset Sale:

Aspect Share Sale Asset Sale What’s Being Sold/ Scope Buyer acquires ownership of shares and gains control of the entire company, including all assets and liabilities. Buyer acquires specific assets and liabilities (e.g. properties, equipment and machinery, etc.). Seller retains the rest. Contract Parties The shareholder and the Buyer. The company itself and the Buyer Tax Implications (For general information only. Please seek professional advice for actual tax implications.)

- May be subject to Capital Gains Tax on gains from the disposal of unlisted shares (if the Seller is a company, limited liability partnership, trust body or co-operative society).

- May trigger Real Property Gains Tax (“RPGT”) (if it’s shares in a real property company).

- Stamp duty may apply on share transfers.

- No stamp duty on individual assets (because no change in asset ownership).

- Ad valorem stamp duty may apply per transfer of asset (land, property, etc.)

- Gains from disposal may be taxable depending on the type of asset:

- Real property → RPGT

- Plant & Machinery / Equipment → Balancing charges (A balancing charge is added when an asset is sold above its tax written-down value.)

Consents & Approvals - Pre-emption rights or tag-along rights may apply

- Change-of-control clauses in contracts may require consent.

- May require third-party consents, novations, assignments and approvals.

- Board/shareholder resolutions may be required if a “substantial portion” of the business is disposed of (Section 223 Companies Act 2016).

Employment No change of employer, employee consent is not required. - No automatic transfer of employees. Employee’s consent will be required.

- Employment procedures, notice periods and termination benefits under the Employment Act 1955 and Employment (Termination and Lay-Off Benefits) Regulations 1980 may be applicable (mainly for employees earning ≤ RM4,000 or manual labour).

* Note: Employees who reject equally favourable terms may lose entitlement to termination benefits.

Due Diligence Considerations - Review corporate records and governance compliance.

- Check litigation, regulatory compliance, and tax filings.

- Investigate related-party transactions and contingent liabilities.

- Verify title and ownership of assets.

- Assess encumbrances or security interests.

- Review assignability of contracts and licences.

- Perform physical inspection of assets.

Warranties & Indemnities - Warranties generally cover all aspects of the target company.

- Indemnities typically for tax, litigation and contingent liabilities.

- Warranties limited to specific assets sold.

- Indemnities are narrower, depending on the asset type and exposure.

Pros & Cons for Buyer and Seller:

Share Sale

Party Pros Cons Buyer - Continuity of business and operations.

- No need to reassign contracts or employees.

- Maintains existing licenses and permits.

- Preserves goodwill and the company’s brand reputation.

- Inherits all existing liabilities (both known and unknown).

- Potential exposure to historical or ongoing litigation or statutory breaches of the company.

- Extensive due diligence is required to uncover potential risks.

Seller - Potentially higher sale price, as the buyer acquires the whole company.

- Clean exit from the business.

- Fewer transfer formalities (i.e. no individual transfer of assets).

- Buyers may demand extensive warranties or indemnities to mitigate risk.

- Potential liability from post-completion claims if warranties/indemnities are triggered.

- Negotiations may be complex due to liability concerns.

Asset Sale

Party Pros Cons Buyer - Can selectively acquire assets and liabilities.

- May avoid unwanted or unknown assets or liabilities.

- Lower risk of inheriting historical or existing litigation or regulatory non-compliance.

- Asset-by-asset transfers can be time-consuming.

- Higher legal, registration, stamp duty and potential tax costs

Seller - Can sell specific assets while retaining core or strategic parts of the business.

- Allows monetisation of certain assets for reinvestment or restructuring.

- Warranties, indemnities and terms can be tailored for each asset.

- The sale price may be lower due to a selective asset purchase.

- Asset-by-asset transfers can be time-consuming.

- Employees don’t automatically transfer — possible claims.

- May retain certain liabilities not assumed by the buyer.

- Tax implications vary by asset.

🔑 Key Takeaway:

Choosing between Share Sale and Asset Sale is more than just a technical decision – it affects your legal exposure, tax implications, operational control and transaction complexity.

In Essence:

Disclaimer: The content of this article is intended for general informational purposes only and does not constitute formal legal advice.

Our Corporate team regularly advises local and international corporations on mergers and acquisitions (M&A), cross-border transactions, joint ventures, and corporate restructuring. We also provide comprehensive support for shareholders’ agreements and general commercial advisory to help businesses navigate the Malaysian regulatory landscape.

For legal assistance or further inquiries regarding your corporate matters, please feel free to contact us.

- January 13, 2026

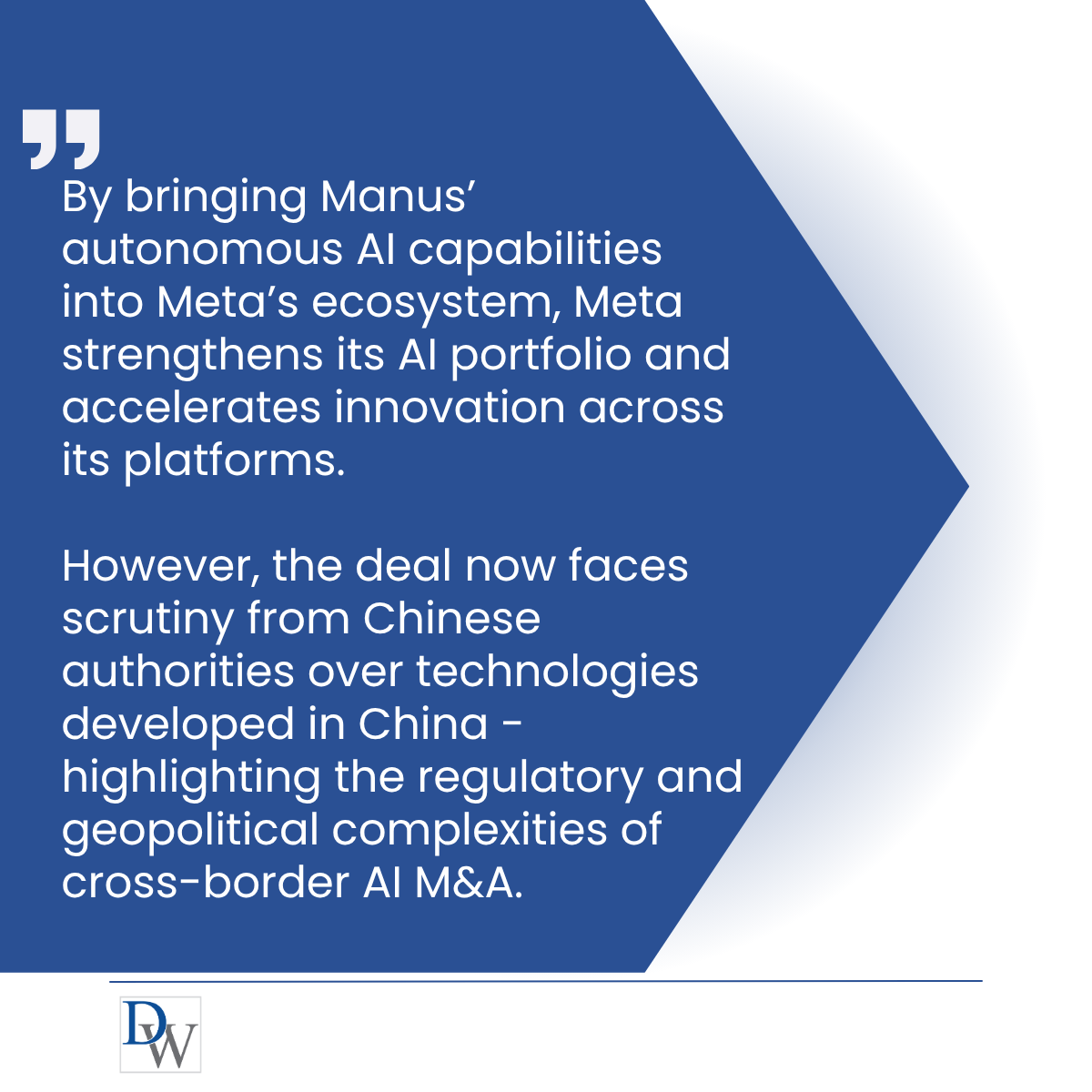

Meta, which operates major social media platforms including Facebook, Instagram, WhatsApp and Threads, has acquired Manus AI, a Singapore-based AI start-up founded by Chinese entrepreneurs, in a transaction reportedly valued between US$2 – 3 billion. Manus is known for its autonomous general-purpose AI agents capable of executing complex tasks with minimal human input, making it a strategic addition to Meta’s AI ecosystem.

The deal has also drawn post-acquisition regulatory scrutiny, with Chinese authorities reviewing whether Manus’s AI technologies developed in China fall under national security or export control regulations, highlighting the geopolitical and legal complexity of cross-border AI M&A.

Taken together, this development demonstrates the strategic potential of autonomous AI acquisitions while highlighting the regulatory and geopolitical risks they entail.

🌏 Follow us for monthly insights into significant M&A deals around the world.

Our Corporate team regularly advises local and international corporations on mergers and acquisitions (M&A), cross-border transactions, joint ventures, and corporate restructuring. We also provide comprehensive support for shareholders’ agreements and general commercial advisory to help businesses navigate the Malaysian regulatory landscape.

For legal assistance or further inquiries regarding your corporate matters, please feel free to contact us.

- December 11, 2025

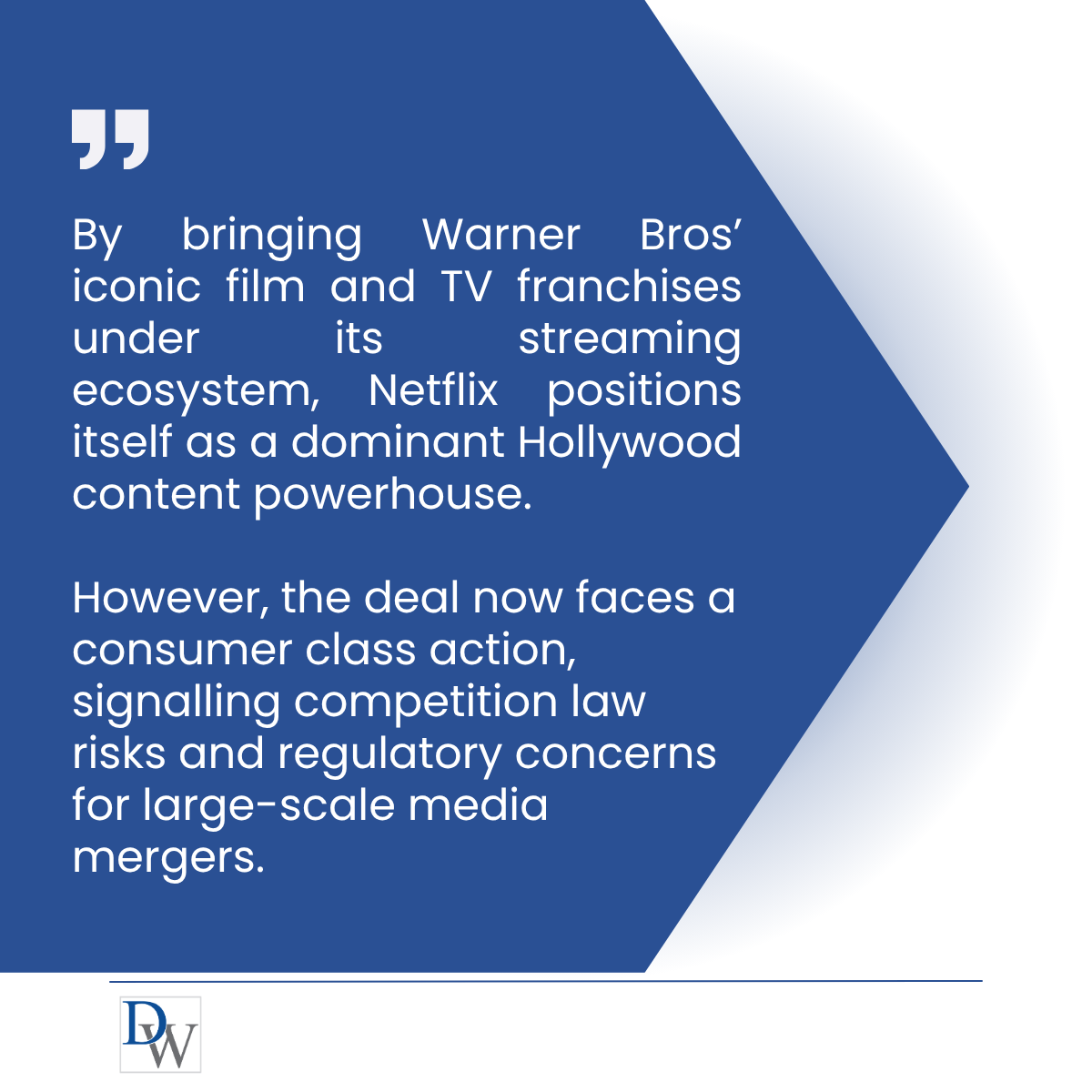

Netflix has recently announced its proposed acquisition of Warner Bros. Discovery, valued at approximately US$82.7 billion (“𝗣𝗿𝗼𝗽𝗼𝘀𝗲𝗱 𝗔𝗰𝗾𝘂𝗶𝘀𝗶𝘁𝗶𝗼𝗻”), merging a content powerhouse with a leading streaming platform and reshaping the global entertainment landscape.

While the Proposed Acquisition marks a landmark moment for the industry, it has also triggered a consumer-led competition law challenge, raising regulatory concerns over market concentration and reduced competition in the US subscription video-on-demand market, particularly through the elimination of HBO Max as a significant competitor of Netflix.

Taken together, this development underscores the heightened regulatory and legal risks associated with mega-mergers in the digital entertainment space.

🌏 With this post, we kick off our 𝐆𝐥𝐨𝐛𝐚𝐥 𝐃𝐞𝐚𝐥 𝐑𝐚𝐝𝐚𝐫 series!

Follow us for monthly insights into significant M&A deals around the world.

Our Corporate team regularly advises local and international corporations on mergers and acquisitions (M&A), cross-border transactions, joint ventures, and corporate restructuring. We also provide comprehensive support for shareholders’ agreements and general commercial advisory to help businesses navigate the Malaysian regulatory landscape.

For legal assistance or further inquiries regarding your corporate matters, please feel free to contact us.

- November 7, 2025

We are delighted to have advised iMedia Asia, a wholly-owned subsidiary of Catcha Digital Berhad, in its acquisition of 100% equity interest in the company behind Malaysia’s leading consumer technology media platform.

Our Corporate and Commercial team supported all legal aspects throughout the transaction, from the legal due diligence exercise to the negotiation and finalisation of the Share Sale Agreement.

The transaction was led by our Corporate and Commercial team, Kenneth Wong, Chermaine Chen, and Gillian Lee, whose collaborative efforts were instrumental in bringing the transaction to a successful fruition.

Congratulations to the Catcha and iMedia team, Eric Tan, Tze Khay Voon, Jacky Tee, Cedric Lee Yitzhen, and Chin Yi Hong on this milestone in expanding the group’s digital media network!

🔗Media coverage: –

- https://www.businesstoday.com.my/2025/11/06/catcha-acquires-local-tech-site-technave-for-rm6-million/

- https://themalaysianreserve.com/2025/11/06/catcha-digital-to-acquire-technave-owner-maxoom-for-rm6-m/

- https://technode.global/2025/11/07/catcha-digital-acquires-technave-for-1-47m-to-strengthen-position-in-consumer-tech-digital-media/

- https://technave.com/gadget/Catcha-Digital-buys-TechNave-for-RM6-125-million-44787.html

- https://newswav.com/article/catcha-digital-acquires-100-of-tech-digital-media-company-technave-for-rm6-A2511_cp1mG6

- https://www.dagangnews.com/article/terkini/catcha-digital-ambil-alih-technave-bernilai-rm613-juta-60558

- https://www.marketing-interactive.com/catcha-digital-continues-acquisition-streak-takes-full-ownership-of-technave

Our Corporate team regularly advises local and international corporations on mergers and acquisitions (M&A), cross-border transactions, joint ventures, and corporate restructuring. We also provide comprehensive support for shareholders’ agreements and general commercial advisory to help businesses navigate the Malaysian regulatory landscape.

For legal assistance or further inquiries regarding your corporate matters, please feel free to contact us.